With the year-end holidays upon us, it’s time for business owners and leaders to keep tax considerations in mind as they plan gifts and parties for clients and employees.

This festive season is traditionally an appropriate time to show appreciation for customers and team members. However, you want to understand how to do this while maintaining tax deductions for your company and without creating tax obligations for your employees.

What Qualifies as a Business Gift?

The IRS defines a business gift as a tangible item that’s given in the course of your trade or business. This usually includes anything of value transferred from one person to another without receiving anything of equal or greater value in return.

Cash and gift cards, which contain a cash-equivalent value, are not considered deductible gifts Additionally, event tickets generally fall into the non-deductible “entertainment” category.

Under IRS regulations, a direct gift is intended for a specific recipient. An indirect gift is intended to be used by a customer’s spouse or family, or by several employees (such as having lunch delivered to a client site).

Client Gifts Tax Deductibility

Deductible client gifts generally must be valued at less than $25 made to an individual customer per year. If, for instance, a small-business client has two partners, you can deduct one $25 gift.

For purposes of the $25 limit, you don’t need to include “incidental” costs that don’t substantially add to the gift’s value. These costs include engraving, gift wrapping, packaging, and shipping. Also excluded from the $25 limit are branded marketing items—such as those imprinted with your company’s name and logo—provided they’re widely distributed and cost less than $4.

There isn’t a specific limit for gifts made to a company that includes all their team members, such as buying a lunch or holiday gift baskets, if the costs are considered reasonable.

To support the deductibility of a gift, you should prepare and retain detailed documentation including:

Cost

Description

Date given

Business purpose and relationship

When planning holiday gifts, it’s important to understand that some organizations have policies that limit their value or prohibit giving them to employees. If you’re unsure, check with your client to prevent a potentially awkward situation.

Deductible Employee Gifts

Non-cash employee gifts are generally deductible, provided they qualify as de minimis fringe benefits. To be a deductible de minimis fringe benefit, the gift’s value should be so small that accounting for them would be unreasonable or impractical, considering the frequency with which the employer provides similar benefits to other employees.

Deductible noncash gifts may include food items, lower-cost tech accessories, occasional theater or sporting event tickets, or similar items.

Cash bonuses, as well as cash equivalents such as gift cards, given as a reward for achieving a milestone, celebrating strong performance, or expressing gratitude for an employee’s performance, is considered part of the employee’s taxable wages. As such, they are subject to payroll withholding and are reported as part of their W-2 income.

Maximizing Deductions for Holiday Parties

Holiday gatherings where you invite employees and their guests are generally fully deductible. If you invite a blend of clients and employees to the same event, it will become partially deductible. To maintain deductibility, it’s important to invite all organization members or a business unit. Also, the party should not be lavish or extravagant.

Changes to Food and Beverage Limits

The 100% deductibility threshold for food and beverage expenses provided by a restaurant to a workplace during calendar years 2021 and 2022 as a COVID-19 relief has expired. In 2023, the pre-COVID 50% deductibility limit has returned.

Contact us if you have questions about potential business tax breaks related to giving client or employee gifts or throwing a holiday party.

Resources | Insights | R&D Capitalization and Amortization Changes Take Effect

R&D capitalization and amortization are here, and we recommend planning as though it’s here to stay. Since the 1950s, businesses that incurred R&D expenses under Section 174 have been able to deduct them as incurred. Unfortunately, the Tax Cuts and Jobs Act (TCJA) of 2017 changed this for tax years starting in 2022. Like many in the R&D Credit and tax accounting spaces, we expected that R&D amortization would be done away with or at least delayed, but while several congressional bills were proposed, none made it through into becoming law prior to the extended 2022 tax filing deadlines of 9/15 and 10/16/2023.

Even though drafts of the Build Back Better Act (BBBA passed in August 2022) did attempt to push R&D amortization out to 2026, those changes did not make it into the final bill. While the deadline may be pushed out with another piece of legislation, at this point we recommend planning for the impact as though it won’t be. Taxpayers taking advantage of R&D expense deductions could be hit with an increased tax liability.

What’s Different About R&D Capitalization

The TCJA legislated that R&D costs must be capitalized and then amortized over a period of 5 or 15 years for domestic and international costs, respectively.

Historically, taxpayers deducted the full amount of their non-capitalized R&D expenses in the year incurred. Starting in tax years beginning after 12/31/2021, this deduction will be spread out over a period of years. This reduces the value of the R&D expenses in the current tax year and can impact taxable income.

R&D Capitalization Broken Down

How it Used to Work

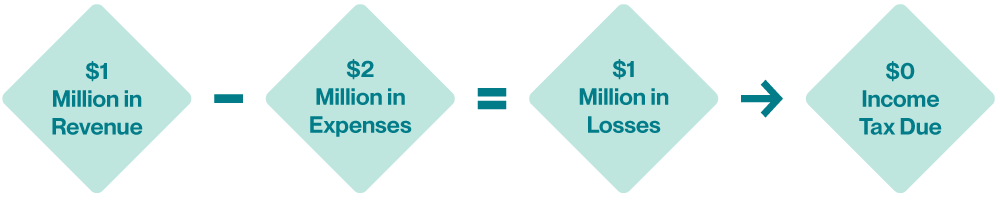

The current process is relatively straight-forward: whatever you expense as R&D, you can write that full amount off for the tax year in which the expenses are incurred. Often this leads to a limited or nonexistent tax bill for start-up companies heavily investing in R&D.

For example, if a company has $1 million in revenue and $2 million in R&D expenses, it will have a net loss of $1 million and therefore do not generate any current year income tax liability.

How it Will Work

Taxpayers who usually depend on R&D expense deductions may be hit with a surprise. They will only be able to write 1/5 of the amount of domestic expenses or 1/15 of expenses for global expense. In addition, because of the requirement to use the mid-year amortization convention, the company will only be allowed half of the deduction in the first year (the other half comes in year 6 or 16).

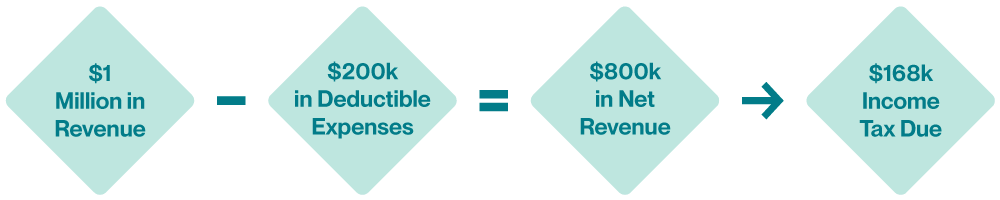

Let’s apply the new guidelines to the same $1 million dollars in revenue and $2 million in US R&D spend used above. Now we must capitalize and amortize, deducting $200,000 in 2022, $400,000 from 2023-2026, and $200,000 again in 2027. In this case, for 2022 our equation is $1 million revenue – $200k amortization = $800k in revenue. At the corporate tax rate of 21%, the income tax due is $168k and has a substantial impact on businesses if not planned in advance. The deduction for the remaining $1.8 million isn’t gone, it’s just spread out over several years.

Note that if a company’s R&D spending is flat, in the 6th year, the carried forward amounts from the 1st – 5th year will add up to the amount that would have been deductible before the change. This effectively creates a “phase-in” period for all companies from 2022 through 2026 and any start-up in their first years.

Old Way

Year

Percentage Use

Amount Generated

Amount Used

2021

100%

$2,000,000

$2,000,000

New Way

Year

Percentage Use

Amount Generated

Amount Used

Year 1

2022

10%

$2,000,000

$200,000

Year 2

2023

20%

$0

$400,000

Year 3

2024

20%

$0

$400,000

Year 4

2025

20%

$0

$400,000

Year 5

2026

20%

$0

$400,000

Year 6

2027

10%

$0

$200,000

NOLs Impact & R&E Credit Impact

The changes to R&D capitalization and amortization will also impact how companies utilize Net Operating Losses (NOLs). NOLs account for how much a business “lost” in a given year. R&D capitalization will reduce the amount of NOL generated because only a portion of R&D expenses will be deducted each tax year.

Section 41 and Section 174

This change makes expenses that qualify for the Research & Experimentation tax credit under Section 41 (R&E Credit, often called the R&D Credit) more valuable. Expenses incurred for the R&E Credit under Section 41 are also includable under Section 174, though the 174 R&D expense definitions are broader and include foreign R&D.

Even though the company can no longer claim all of deduction for the Section 174 R&D expenses in the year incurred, they can still include any eligible expense for that year’s Section 41 R&E credit. While the deductions are applied to the revenue, the R&E credit is applied after corporate taxes are calculated, resulting in dollar-for-dollar reduction in the tax owed. Any credits not used in the year generated can be carried forward indefinitely.

Additionally, beginning in tax year 2021, any NOL generated can only be used to offset 80% of taxable income in future years. Companies who would have historically been able to use NOL carryforwards and R&D expense deductions to reduce their tax liability will be doubly impacted by these changes starting in 2022.

Continuing the example from above, the $2 million in R&D expenses would generate an R&E credit of as much as $200k (20% credit on expenses over a threshold of at least 50% the expenses, so 20% of $1M excess qualified research expenditures (QREs)). With that same $168k bill, the R&E credit can now bring the tax bill back down to $0, and carry forward $32k into future periods.

The One Big Beautiful Bill Act was signed into law in July 2025. It repeals the mandatory domestic portion of Section 174 capitalization and amortization for tax years starting after December 31, 2025. The international portion remains unchanged.

Since Congress has not agreed to restore capitalization and amortization of Section 174 R&D expenses from mandatory to elective, the IRS has authorized an automatic approval process for the change in accounting methods process required.

Rev. Proc. 2023-11outlines the process the IRS uses instead of the waived Form 3115, Application for a Change in Accounting Methods. Under this process, each taxpayer must submit a statement with the return in lieu of the Form 3115 (including the duplicate copy filing):

Taxpayer name and ID

Beginning and end dates of the year of change. Typically, this will be the taxpayer’s tax year 2022

The designated Automatic Accounting Method Change number under section 7.02(8): 265

A description of the expenditures included as specified R&D

The amount of expenditures included in item 4

A declaration that “[Taxpayer] is changing the method of accounting for specified research or experimental expenditures to capitalize such expenditures to a specified research or experimental capital account, and amortize such amount over either a 5-year period for domestic research or 15-year period for foreign research (as applicable) beginning with the mid-point of the taxable year in which such expenditures are paid or incurred in accordance with the method permitted under § 174 for the year of change. [Taxpayer] is making the change on a cut-off basis.”

The amounts identified are then entered on form 4562 – Depreciation and Amortization part VI and the associated schedules.

Help Unraveling the R&D Expense Capitalization Puzzle

Do you think the changes to R&D capitalization and amortization might impact you? Contact our team to learn about potential impacts and planning opportunities.

Resources | Insights | R&D Payroll Tax Credit Election for Small Businesses

The tax credit for increasing research activities, often referred to as the research and development (R&D) credit, offers a valuable incentive to eligible businesses.

In addition to the credit itself, there are two features especially favorable to small businesses:

Businesses with $50 million or less in gross receipts may claim the credit against their alternative minimum tax (AMT) liability.

The credit can be used by certain smaller startup businesses against the employer’s Social Security and Medicare payroll tax liabilities.

Let’s look at the second feature. Subject to limits, you can elect to apply all or some of any research tax credit against your payroll taxes instead of your income tax. This payroll tax election may influence your decision to undertake or increase your research activities.

Why the Election Is Important

Many new businesses, even if they have some cash flow, net positive cash flow, or a book profit, pay no income taxes and won’t for some time. In these cases, there’s no amount against which business credits, including the research credit, could be applied.

On the other hand, every wage-paying business has payroll tax liabilities.

Therefore, the payroll tax election is an opportunity to get immediate use out of the research credits you earn. Because every dollar of credit-eligible expenditure can result in as much as a 10-cent tax credit, that’s a big help in a company’s start-up phase.

Eligible Businesses

To qualify for the election, a taxpayer must:

Have gross receipts for the election year of less than $5 million, and;

Be no more than five years (or tax periods) past the period for which it had no receipts (the start-up period).

In making these determinations, the only gross receipts that an individual taxpayer considers are from the individual’s businesses. An individual’s salary, investment income, or other income aren’t considered. Also, note that an entity or individual can’t make the election for more than five taxable periods in a row.

Limits on the Election

The election must be made on a live, timely-filed return (including extensions), not on an amended or late filing. The credit can then be claimed on the payroll filing starting the quarter after the tax return is filed. If a taxpayer filed their 2022 return on April 15, 2023 (during Q2), they could start using the amounts in Q3 2023.

Starting with the 2023 tax year, limits on the amount of research credit for which the election can be made can’t exceed $500,000, doubling the $250,000 limit in place before 2023. The payroll tax offset can be elected in any amount up to the amount of total credits generated or the statutory maximum.

Another change that started in 2023 is that the research credit for which the taxpayer makes the payroll tax election can be applied to the employer side of Social Security and Medicare, not just the Social Security portion of FICA taxes.

The above are just the basics of the R&D payroll tax election. Keep in mind that identifying and substantiating expenses eligible for the research credit itself is a complex area. Contact us about whether you can benefit from the payroll tax election and the research tax credit.

Resources | Insights | Choosing the Right Trust Services Criteria for Your SOC 2 Audit

A SOC 2 audit is like a report card that shows clients you’ve got your act together when it comes to handling their sensitive information. It’s proof that your systems and processes have been thoroughly checked and approved by objective, third-party experts.

What’s unique about a SOC 2 report is that you get to define the scope. Every service organization gets evaluated on security, but choosing the other security and privacy considerations that get audited—known as the Trust Services Criteria—is up to you.

Which Trust Services Criteria Should You Choose?

The Trust Services Criteria are a set of five IT security principles developed by the American Institute of Certified Public Accountants (AICPA) to help organizations safeguard their sensitive information and assets.

In this article, we’ll outline each Trust Services Criteria category and provide guidance on whether you should consider including it in your SOC 2 scope.

Security

The security category focuses on protecting information and systems from unauthorized access, use, disclosure, disruption, modification, or destruction. This includes protecting systems both physically (on location) and from remote threats like hacking, viruses, and other cyber attacks.

Important security-related controls and processes include the use of passwords, authentication systems, segregation of duties, encryption, and firewalls.

Security is required for all SOC 2 reports and, therefore, is sometimes referred to as the “common criteria.”

Availability

Availability means ensuring information and systems are accessible to authorized users when needed. This includes minimizing downtime and maintaining system performance. Relevant controls may include redundant servers, backup and recovery systems, load balancing, and disaster recovery plans.

If you answer “yes” to any of these questions, consider including availability in your audit scope:

Do you have service level agreements (SLAs) related to system uptime or performance?

Would system downtime significantly impact your customers’ operations?

Processing Integrity

When looking at processing integrity, auditors want to know your systems are handling information accurately and reliably, without experiencing errors, omissions, incorrect processing, or unauthorized or accidental manipulation.

If you answer “yes” to any of these questions, consider including processing integrity in your audit scope:

Do your customers rely on your systems to perform critical operational tasks like financial or data processing?

Would inaccurate or unreliable data produced by your systems negatively impact customers?

Do you transform, manipulate, or analyze customer data in your systems?

Confidentiality

Here, auditors are looking at how you protect information designated as confidential. This may include trade secrets, intellectual property, or client financials. Confidentiality controls may include data classification rules that govern who can access certain information.

Examiners may also ask about audit trail capabilities, meaning your ability to monitor who accessed sensitive information and what actions they took (e.g., copying, deleting, or editing data).

If you answer “yes” to any of these questions, consider including confidentiality in your audit scope:

Do you handle sensitive data protected by NDAs or regulations?

Do you collect and store intellectual property, trade secrets, or client financials?

Do your contracts with customers require you to delete their data when no longer needed?

Privacy

Privacy specifically focuses on controls to protect personally identifiable information (PII). Auditors will be looking to see if you operate in accordance with client agreements, as well as any applicable laws or regulations.

Privacy controls often include issues of notification, choice, and consent. This means you’ve let people know how you collect, use, and retain their information so they can make an informed decision about whether to share it with you.

Privacy criteria may also deal with issues of access, such as giving customers a way to view the information you’ve collected so they can ask you to correct it. In addition, auditors will be looking at your disclosure and notification policies, such as defining how you’ll detect data breaches and notify customers if a breach occurs.

If you answer “yes” to any of these questions, consider including privacy in your audit scope:

Do you collect PII from customers such as Social Security numbers, birthdays, or healthcare data?

Do you need consent management tools to collect customer PII?

Are you subject to data privacy regulations such as the European Union’s General Data Protection Regulation (GDPR) or the California Consumer Privacy Act (CCPA)?

Choose the Trust Services Criteria Your Customers Expect

Evaluating your customers’ key concerns will help determine which Trust Services Criteria to include in your SOC 2 audit. A more comprehensive audit can demonstrate a stronger commitment to security and satisfy a greater number of potential customers.

Our goal is to make your SOC 2 audit as straightforward as possible, with a practical approach that addresses your concerns in a cost-effective manner. For more information and help defining your SOC 2 audit scope, get in touch with our team.

Resources | Insights | Getting Your BlackLine Admins Prepared for 2024

As BlackLine administrators and finance leaders prepare to roll their instance into 2024, the end of the calendar or fiscal year requires some important steps and provides a great opportunity to review, update, and optimize your system settings.

Perhaps the first and most important item on your year-end to-do list is adding monthly, quarterly, and annual period end-dates for the coming calendar year. Be sure to indicate which periods are quarter-ends or the fiscal year-end.

If you skip this step, system imports will fail and users won’t be able to choose the proper period to complete their assignments. As you prepare these dates, it’s a good practice to only add period end-dates for one year at a time so users don’t have to scroll through lengthy menus to find the current-year periods.

Assign Due Dates

As a related step, it’s vital to assign due dates for the routine tasks within each period. This will usually include reconciliations, variance, and BlackLine’s consolidation integrity manager (CIM). If the due dates are left blank, users won’t see when their assignments are due and may not complete them on time. This failure can also delay the close process.

Forgetting to include due dates will also impact any alerts or notifications you’ve turned on and will prevent you from running reports based on late or past-due statuses for reconciliations, variance, or CIM because there isn’t a due date for BlackLine to use in its calculations.

Close Prior Periods

It’s also important to make sure all prior periods have been closed for importing balances. Ideally, this should take place monthly. Failing to close periods can allow transactions with incorrect dates to be imported into a prior period. This, in turn, will overwrite balances for your reconciliations and trigger corrections that will require documentation and could lead to questions from your external auditors.

Check Custom Frequencies

If your BlackLine instance includes custom frequencies, such as a frequency other than monthly for a given module, you’ll need to assign the correct period end-dates to the corresponding frequencies. For example, the 12/31 period will commonly be assigned to monthly, quarterly, and annual frequencies, and will likely have assigned tasks, variances, or reconciliations for each of those periods.

Review Your Matching Module

Year-end is a great time to review your matching module settings to identify any unloaded transactions that need administrative action, or unmatched transactions and posting dates outside of your organization’s tolerance. It’s also a good time to review your matching rules to ensure they’re performing properly.

For instance, a rule that has not captured any transactions may need to be adjusted, or perhaps it can be eliminated. Having outdated or unnecessary rules in the system can increase the job time of the matching engine, so it’s helpful to review your settings and rules periodically.

Other Items to Review

It’s a best practice to review the following settings as you prepare for a new year:

Administrative Tasks

List any steps and documentation associated with administrative tasks. It’s easy to overlook tasks that are only done once per year. Providing screenshots and other completion documentation can help you answer any audit-related questions.

First Transaction Imports

Monitor your first transaction imports. Be sure the dates on the files are rolling over successfully into the new year.

User Roles and Access Rights

People and roles change over the course of the year and you want to be sure everyone has the appropriate access (and that you’re not paying for licenses that aren’t being used).

Account Settings

Review the account settings for reconciliations due to groupings or account rules. Be sure the new year’s due dates are aligned with management expectations.

Organization’s Holiday Calendar

Upload your organization’s holiday calendar into BlackLine to ensure due dates are calculated correctly. If January 1 is an organizational holiday, for instance, you don’t want users to start the first business day of the new year with notifications that tasks are overdue. If you have questions about closing out your fiscal year or optimizing your BlackLine implementation, contact us.

We can help you streamline your transition into the new year and avoid common mistakes that can lead to issues later. Beyond questions, our no-cost BlackLineBoost assessment will review your settings and help you harness BlackLine’s powerful tools more effectively

Resources | Insights | 5 Common Mistakes to Avoid Before Starting a SOC 2 Audit

A SOC 2 report can be a powerful tool in demonstrating your company’s commitment to securing your customers’ data. And while the benefits are compelling, several common mistakes or misunderstandings about SOC 2 audits can make the process more complicated, lengthy, and expensive.

A SOC 2 compliance report summarizes the results of an external auditor’s evaluation of your company’s policies, processes, and controls for protecting customer data in five key areas:

Security

Availability

Processing integrity

Confidentiality

Privacy

A SOC 2 Type 1 report tests control designs at a specific point in time, while a more comprehensive Type 2 report tests controls repeatedly over a period of time to confirm operating effectiveness.

Customers depend on the SOC 2 audit results as they conduct due diligence on prospective and current cloud service vendors. They want assurance they can safely integrate their internal and customer data. SOC 2 compliance is an important consideration or requirement for many companies as they choose technology partners.

5 Common SOC 2 Audit Mistakes

The following five mistakes can complicate the SOC 2 audit process or hinder your ability to take advantage of the assurance a SOC compliance report offers your customers.

1. Not Designating a Project Manager

As you’re planning for a SOC 2 audit, naming a project manager is essential in streamlining the flow of information within your organization and with your external auditor. A SOC 2 audit’s broad scope means you will collect information and documentation from business functions, including HR, operations, systems admins, database professionals, and others.

Each control will require someone with subject matter expertise to provide evidence of that control’s effectiveness for the auditors to review. If you don’t designate someone to coordinate that information flow, the auditors must track down documentation function by function. This complex process will extend the life of the project considerably.

Instead, choosing a single point of contact can make this process faster and more efficient. If you do not have someone with project management experience on staff, consider bringing in an external project manager on a consulting basis.

2. Not Performing a Readiness Assessment

Before you engage an auditor, it’s crucial to conduct a readiness assessment to identify the controls that will be examined during the audit, any missing controls, and any controls that lack documentation.

Failing to perform these basic steps before the audit begins can easily lead to unexpected control gaps and failures during the audit that, in turn, can hamper your ability to obtain a report documenting SOC 2 compliance. As with project management, a consultant with readiness assessment expertise can help streamline the process and enhance your capabilities.

3. Not Performing Interim Testing During an Audit

It’s important to test your controls during the first reporting period covered by your SOC 2 assessment. For instance, if you’re performing an audit based on six months, you should test your controls after three months to ensure they have been operating effectively for that timeframe.

This interim testing allows you to identify and mitigate any control exceptions, so you’d have the rest of the period for that control to operate effectively. Interim testing is optional, but it’s far more effective than waiting for the end of the period and discovering deficient controls that force you to extend the review period as you mitigate issues.

4. Expecting Customer Security Questionnaires to Stop

Although most clients who ask about your information-protection policies and controls will be satisfied with a SOC 2 report, companies with security questionnaires will likely continue to issue them. Because each company’s operating environment (and questionnaire) are different, merely handing over a SOC 2 report is unlikely to satisfy their request for information. You may be able to pull information from the report in answering the questionnaire, but don’t expect questionnaires to become a memory.

5. Assuming SOC 2 Is One and Done

When you receive a SOC 2 compliance report, that doesn’t mean the process is over. Effective risk management is an ongoing process, which means that, for subsequent periods, you’ll have to stay on top of the controls and operations covered in the initial report.

This will require ongoing risk assessments, updating policies and procedures as changes occur in your environment, vulnerability scanning and penetration testing, updating business continuity and disaster recovery plans, and other assessments.

By avoiding these common mistakes, you’ll receive a SOC 2 report demonstrating your commitment to securing and protecting customer data and a report you’ll be pleased to hand to any prospect or customer who asks for one.

Need help preparing for your SOC 2 audit? Contact us.

Resources | Insights | How to Read a SOC Report in 5 Minutes (or Less)

TL;DR: Open the SOC report, click Ctrl+F, and search for “Opinion.” If the audit opinion states, “In our opinion, in all material respects …” the report gets a gold star. See? That was even less than five minutes!

After performing SOC audits day-in and day-out and issuing hundreds of SOC reports to clients, it recently occurred to me that I may take for granted that everyone knows how to determine if a SOC report was a “pass” or a “fail.”

I’m not saying you shouldn’t read the entire SOC report, because you should; there’s a lot of essential and detailed information in those reports, but let’s be honest—reading that 100-page report could take some serious time. So, as an alternative to reading every page, there is an easy and quick way to summarize the results of a SOC 1 or SOC 2 report, and there are a few variations of “pass” and “fail.” Let’s clear those up first, then I’ll tell you exactly where to find them in the report.

“Pass” and “Fail” Opinions

Unqualified Opinion

The best outcome for the SOC report is when the audit firm states an “unqualified opinion.” This simply means the auditors have determined that the organization under examination can achieve its service commitments and system requirements as described in the report. This is also known as a “clean opinion,” which everyone wants to see. The unqualified opinion will use the following language: “In our opinion, in all material respects …”

Qualified Opinion

The second level of pass is in the form of a “qualified opinion.” This isn’t a bad thing, but it’s not a clean opinion either. A qualified opinion means the audit firm has determined that some controls at the organization aren’t designed well or aren’t operating as they should be. These can be minor and correctable (and explainable) issues that organization management acknowledges and has a reasonable plan to correct.

No one’s perfect, and a slip in control can happen from time to time. If you see a qualified opinion, you’ll want to dig deeper into the report to evaluate what “exceptions” were found by the auditor and management’s remediation plan. The qualified opinion will use the following language: “In our opinion, except for the matter referred to in the preceding paragraph …”

Adverse Opinion

The third type of opinion would move into the failure column. This is when the audit firm issues an “adverse opinion” in the report. This typically means the system description was not presented accordingly, the controls were not appropriately designed, or they did not operate effectively—all meaning that the organization would have trouble meeting its service commitments and system requirements.

This opinion should give you pause if you’re relying on that organization to provide any service to your business. The adverse opinion will use the following language: “In our opinion, because of the matter referred to in the preceding paragraph …”

Disclaimer Opinion

The fourth and final opinion, is the dreaded “disclaimer of opinion.” This is the unicorn of SOC reports—it’s so rare that I’ve never seen one (and our firm has never issued one). But you can probably guess why these are never seen—what organization would ever distribute this version of their SOC report? A “disclaimer of opinion” means the audit firm has concluded that they could not validate if any of the controls were operating during the reporting period and were unable to complete the audit.

Where to Find the Auditor’s Opinion

Where can we find the auditor’s opinion in the report? There are typically four sections of the report and you will want to locate the section titled “Independent Service Auditor’s Report.” This is usually either Section I or Section II of the report.

Once you find the auditor’s report section, scroll down to the “Opinion” section. Here’s where you’ll find out if the report is a pass or fail. Again, if the opinion is unqualified, you can put the report down with confidence and enjoy that second cup of coffee. If it’s any of the other opinions we discussed above, you’ll probably want to dig deeper into the details to learn what the findings mean.

I’m a visual person, so keep this in mind when reviewing the auditor opinions:

Unqualified Opinion =

Qualified Opinion =

Adverse Opinion =

Disclaimer Opinion =

For more information or help preparing for your SOC audit, please get in touch with our team.

“Whycan’t I share my SOC 2 report?” It’s a question we’re asked a lot, and given the time and expense of acquiring a SOC 2 report, it’s understandable. You can share it, but your report is restricted and there are good reasons behind this restriction.

SOC 2 Is a Restricted Use Report

The SOC 2 report is, by definition, a restricted use report. As such, it’s not suitable for public distribution. If you think about it, a SOC 2 report includes a detailed system description and a matrix of controls specific to your company that often includes proprietary information. From a process and security stance, it makes sense not to publish this information for your competitors or people with nefarious intentions to see. This is why if you do a Google search for “example SOC 2 report”, you can’t easily find one.

Suppose you use AWS or Microsoft Azure as your subservice organization and need a copy of their SOC 2 report. In that case, there’s a specific process to verify whether you should be given access to this information. Further, the AICPA standards look to the “intended reader” of the report and whether that reader has sufficient knowledge to understand the report’s content.

Case in point: The following excerpt is standard audit opinion language that appears in all SOC 2 reports detailing “Restricted Use.” You’ll notice that it reinforces the AICPA’s “intended reader” standards:

This report, including the description of tests of controls and results thereof in the section of our report titled “Description of Test of Controls and Results Thereof” is intended solely for the information and use of [Service Organization Name]; user entities of [Service Organization Name]’s [insert title of the description] during some or all of the period [Month XX, 20XX] to [Month XX, 20XX], business partners of [Service Organization Name]’s subject to risks arising from interactions with [Service Organization Name]’s processing system; practitioners providing services to such user entities and business partners; prospective user entities and business partners; and regulators who have sufficient knowledge and understanding of the following:

The nature of the service provided by the service organization.

How the service organization’s system interacts with user entities, subservice organizations, and other parties.

Internal control and its limitations.

Complementary user entity controls and complementary subservice organization controls and how those controls interact with the controls at the service organization to achieve the service organization’s service commitments and system requirements.

User entity responsibilities and how they may affect the user entity’s ability to effectively use the service organization’s services.

The applicable trust services criteria.

The risks that may threaten the achievement of the service organization’s service commitments and system requirements and how controls address those risks.

This report is not intended to be and should not be used by anyone other than these specified parties.

The Difference Between SOC 2 vs. SOC 3

For more general use, a SOC 3 report is an optional add-on for a SOC 2 report that omits detailed control listings and sensitive information and employs modified system descriptions. In effect, it is a summarized version of the SOC 2 Type 2 report. As such, it is defined as a “general use report” and can be distributed freely.

In contrast to the challenges of obtaining Amazon or Microsoft’s SOC 2 reports, both share their SOC 3 reports publicly.

For more information on why SOC 2 reports are restricted use and examples of other, more general alternatives, check out the AICPA’s guidance on the available SOC reports. If you’re considering a SOC 2 report, don’t hesitate to reach out to our team or visit our SOC 2 services page.

Resources | Insights | From 529 to Roth IRA: New Opportunities for Families

Families concerned they may have been saving too much for their children’s education qualified tax-advantaged tuition “529” plans have greater flexibility and financial opportunities thanks to changes under the SECURE 2.0 Act.

Beneficiaries are now given the option to roll unspent education funds into Roth IRA retirement savings accounts. The ability to convert 529 plan funds to a Roth IRA provides more options for utilizing educational savings and generating long-term, tax-free growth.

Under the old regulations, leftover funds that were not withdrawn and used for qualified educational expenses were subject to income tax on the earnings portion of the withdrawal as well as a 10% penalty. The potential penalties were widely considered impediments to the broader adoption of 529 college plans.

Parents were concerned about children who might not be interested in pursuing higher education or who may not need the 529 funds if they qualified for attractive financial assistance. Some families invested conservatively or bypassed 529 plans altogether.

Retirement Savings Opportunity

The ability to make tax-free transfers of unused educational funds into retirement savings, starting in 2024, will make 529 plans more attractive to plan owners (typically parents) and beneficiaries (usually their children).

However, there are several restrictions that plan owners and beneficiaries must understand:

The Roth IRA must be in the name of the beneficiary, not the plan owner.

Rollovers are subject to annual Roth IRA contribution limits. For 2023, this amount is $6,500.

There is a lifetime rollover limit of $35,000 that can be transferred from a 529 to a Roth IRA.

The 529 plan account must have been open and held for the designated beneficiary for at least 15 years.

Rollover funds cannot exceed the contributions to the 529, or earnings on those contributions, made in the previous five years.

Families With Multiple Children

Families with multiple children often fund separate 529 plan accounts for each child. Under the old rule, parents could transfer any leftover funds in one child’s account to another child, thereby sharing the education savings among their children. While this remains an option, parents should consider the new 529 transfer rule before transferring funds between accounts.

Under the new 529 transfer rule, a tax-free transfer can only be made into an account of a designated beneficiary that has been maintained for at least 15 years. The IRS has not yet issued guidance on whether changing the beneficiary of a 529 plan from one child to another resets the 15-year clock.

One option is for the plan owner to request a rollover of funds from one child’s account to another while leaving the initial account open in the name of the original beneficiary, thereby avoiding a potential reset of the 15-year clock.

Potential State Tax Consequences

If a proposed rollover occurs between accounts established in different states, plan owners also need to investigate potential state consequences.

One example of these consequences is clawbacks of deductions taken in the state from which funds would be transferred. Such clawbacks may not preclude a rollover, but owners should understand and plan for any state tax implications.

If you have questions or need guidance on the tax advantages and implications of converting a 529 plan to a Roth IRA, feel free to get in touch with us.

Resources | Insights | Cash vs. Accrual Accounting: What’s Best for Your Business?

One of the most important financial reporting decisions new and growing companies need to make is whether to use cash vs. accrual accounting for their financial records. Each approach offers potential advantages and disadvantages for companies in different situations. Choosing the best method for your company depends on understanding your needs and financial reporting goals.

Under cash-basis accounting, companies recognize revenue as customers pay for purchased goods and services. Similarly, they recognize expenses as they pay for them. This method, often used by small businesses and sole proprietorships, is usually favored for its comparative simplicity.

Under accrual-basis accounting, revenue and expenses are recorded when transactions occur, not when cash is received or spent. By including accounts payable, accounts receivable, and other accounts, accrual accounting provides a more accurate view of a company’s finances that conforms with Generally Accepted Accounting Principles (GAAP). An additional consideration is that companies that have averaged gross receipts in excess of $25 million over the past three years are required to use accrual accounting for income tax filings.

Advantages and Disadvantages of Cash-Basis Accounting

The primary advantage of cash-basis accounting is its simplicity. The company recognizes revenue as it receives cash, and records expenses as they are paid. This approach is easy to understand and may be suitable for companies that do not have financial reporting or management capabilities.

Cash-basis accounting helps a company understand clearly how much cash it has on hand. This can be helpful for a business with tight cash flows. Cash-basis accounting may also provide potential tax benefits by allowing a company to delay the recognition of revenue into a future period and accelerate deductions into a current period.

As a potential disadvantage, cash-basis accounting can provide an inaccurate picture of a company’s financial health and performance. It fails to account for upcoming expenses or revenue.

For example, the finances of an agricultural company may be difficult to assess accurately because it records most of its expenses when crops are planted, and most of its revenue as those crops are harvested. This challenge can be accentuated when revenue and expenses tend to fall within different reporting periods.

Cash-basis accounting also does not conform with GAAP. This can be an issue if the company seeks loans or outside investments.

Advantages and Disadvantages of Accrual-Basis Accounting

Because it includes both prior and future transactions, accrual accounting provides a more accurate picture of a company’s financial performance and health. Accrual offers a more consistent view of a business’s finances by recognizing revenue and expenses as they’re incurred. This can help management prepare more accurate financial reports and forecasts.

Similarly, accrual accounting enables companies to track asset and liability accounts that wouldn’t be included under cash-basis accounting, such as prepaid expenses, work in progress, accounts payable, accounts receivable, and others.

Accrual accounting complies with GAAP, which is required for publicly traded companies and is usually preferred by banks and outside investors. It provides more accurate information for internal management to make better business decisions.

A potential disadvantage of accrual-basis accounting is its relative complexity compared to cash accounting. The company needs finance professionals who understand accounting principles and may need outside accounting assistance to support its financial reporting needs.

Comparing the Two Accounting Methods

Choosing the best accounting approach for your company depends on several factors, starting with the size and complexity of your organization. A smaller company with simple transactions, for instance, may find cash-basis more suitable. Medium-sized businesses with more complex operations, or that plan to attract outside investors, may prefer accrual basis.

Similarly, a company that is public, or is considering going public, will need to comply with GAAP and related regulatory standards (including the use of accrual-basis accounting).

Tax considerations can also play a role in deciding whether a company should adopt cash or accrual accounting. Timing the recognition of revenue and expenses in different periods may affect an organization’s tax liabilities.

Cash-basis accounting is usually less expensive to implement and maintain, but may not provide the detailed insights into the company’s financial results that more complex businesses need.

There are several reasons for a small business to adopt the accrual method of accounting, including reduced financial reporting variability and the ability to attract financing from lenders and investors who prefer GAAP financials. If your company is eligible for the cash method for tax purposes, you may prefer the simplicity and the flexibility it offers.

Whichever method a company chooses, it’s important to follow that accounting basis consistently. For instance, a company that uses cash-basis accounting, but starts to accrue unpaid invoices, can create a misleading picture of its finances and its performance.

Contact us to discuss your questions related to cash vs. accrual accounting methods and let us help you make the optimal choice for your situation.

To develop solutions for a brighter future, sustainability must be intertwined with innovation and development. Using sustainability as a guiding principle is vital in research and development (R&D). Sustainability, as defined by the United Nations, involves meeting the needs of the present without compromising the ability of future generations to meet their own needs. This approach is important for addressing the biggest challenges humanity faces.

R&D activities often have direct or indirect impacts on the environment and society. By integrating sustainability into R&D practices, we can protect essential resources for current and future generations, advance social and economic equity, and contribute to global efforts to combat climate change and protect biodiversity.

Through responsible R&D, environmental and social responsibility can be achieved harmoniously alongside economic viability. This is because sustainability drives long-term vitality for companies while inspiring innovation and competition throughout the industry.

By leveraging science and technology, companies can develop products that have a positive effect on the world and reduce negative impacts. Furthermore, the integration of sustainability into product development (rather than as an afterthought), can ultimately reduce costs and time investment by fostering the efficient use of resources.

The Future of R&D and Sustainability

Technological advancements and innovation will be pivotal in rapidly implementing sustainable practices and policies to meet the 17 Sustainable Development Goals (SDGs) set by the United Nations. As mankind progresses, there will be a shift toward a circular economy where waste is minimized and resources are repurposed efficiently and recycled whenever possible.

It Definitely Won’t Be Easy …

Adding sustainability as a key objective brings significant challenges. While sustainable practices are often cheaper in the long run, there are higher upfront costs and limited funding often constrains sustainable product development. Additionally, focusing on short-term financial gains in some industries may lead to reluctance to adopt sustainable practices as organizations prioritize immediate profits over long-term sustainability investments.

Overcoming these financial hurdles requires a mindset shift to recognize sustainability as an essential and value-enhancing aspect of R&D rather than an additional cost burden.

There’s rarely an easy solution when it comes to sustainability. Every decision involves a trade-off where harm is mitigated in one alternative but may cause an unintended harmful effect elsewhere. For example, electric vehicles can help reduce greenhouse gases over their lifetime but can cause environmental and social harm in certain communities as precious metals are mined for use in batteries.

Finally, data availability and the complexity of global supply chains present obstacles that require careful consideration and strategic collaboration. As the world becomes more interconnected, supply chains often span multiple countries and involve diverse stakeholders. Achieving sustainability in this context requires strategic collaboration among all parties involved, including suppliers, manufacturers, distributors, and consumers.

… But It Will Be Worth It

Despite these challenges, the benefits can be substantial. By prioritizing sustainability, we can help ensure cleaner air and water, optimize resource allocation and provide better living conditions and social equity—all with long-term economic growth in mind.

Moreover, organizations that interweave sustainability into R&D gain a competitive edge. It helps differentiate them in an increasingly environmentally conscious and aware market.

Strategies for Optimizing Sustainability in R&D

To practice sustainable R&D, companies can incorporate the following strategies:

Ensure sustainability is a core component of R&D strategy by setting clear goals and aligning them with the overall business objectives.

Prioritize using sustainable materials and processes while exploring eco-friendly alternatives to current practices.

Apply lifecycle thinking to understand the full impact of products or technologies. This means looking at every stage of a product’s life, from raw material extraction to end-of-life disposal.

Use renewable energy sources to drive down the environmental impact.

Train R&D teams on sustainability and foster a culture of continuous improvement.

The R&D Tax Credit and Sustainability

The Research and Development Tax Credit can be a valuable benefit for any company engaging in product development. Incorporating sustainable practices into the R&D process will likely pay off in various ways during the product lifecycle and result in a larger R&D credit now. While the R&D credit doesn’t provide a direct incentive to incorporate sustainable design, the additional effort required to incorporate these practices can indirectly result in a larger credit due to the additional upfront cost of prioritizing sustainability and lifecycle thinking.

Integrating sustainability into R&D is essential to meet sustainable development goals and provide for the well-being of current and future generations. Through technology, we can create innovative solutions that benefit the environment and society, drive growth, and support economic vitality.

To manage your company’s emissions and plan reductions, you must first be able to quantify those emissions and identify their sources. The best tool for accomplishing these goals is a Greenhouse Gas (GHG) accounting inventory, which helps organizations identify opportunities for waste or cost reductions, respond to stakeholder inquiries, and prepare for changes in evolving regulatory requirements.

To the last point, the EU’s Corporate Sustainability Reporting Directive (CSRD) will require approximately 50,000 companies, including small and medium enterprises (SMEs), to start issuing sustainability reports in 2024. Additionally, the recent harmonization of ISSB standards has seen the publishing of IFRS S1 and IFRS S2, providing climate-related reporting and disclosure guidance.

Demonstrating credible contributions to climate action can also provide an advantage when seeking access to capital or differentiating your brand in a crowded marketplace.

What Is GHG Accounting?

GHG accounting is the process of measuring the emissions resulting from your company’s operations. Standardized methodologies for GHG accounting, developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), are delineated in the GHG Protocol: A Corporate Accounting and Reporting Standard. The first edition of the standard was published in 2001, with the Scope 3 Corporate Value Chain released in 2011.

The Greenhouse Gas Protocol is currently undergoing a governance restructuring to update their standards, with a goal of finalization in 2025. The intent is to ensure standards and guidance can offer a rigorous and credible accounting foundation. The International Organization for Standardization (ISO)’s 14064-1 is another framework that provides technical guidance at the organizational level for quantifying and reporting GHG emissions and removals.

The GHG Protocol Accounting Standard covers six greenhouse gases from the Kyoto Protocol. These gases are:

Carbon dioxide (CO2)

Methane (CH4)

Nitrous oxide (N2O)

Hydrofluorocarbons (HFCs)

Perfluorocarbons (PCFs)

Sulphur Hexafluoride (SF6)

Setting Boundaries

Boundaries are beneficial for pursuing the elusive work/life balance, and crucial to the GHG accounting process. The process begins by determining organizational boundaries – the businesses and operations owned or controlled by the company. This is particularly salient for companies that have jointly owned or controlled entities. Deciding on an approach to boundary-setting will delineate which operations, and what percentage of those operations, should be included.

Organizational Boundaries: Equity Approach Method

Companies must choose an equity share approach or a control approach. If an organization proceeds with the equity approach, they apply the percentage of equity share to calculate the company’s share of operations. For the control approach, there are two pathways: financial or operational control.

Financial Control Method

The financial control approach is predicated on the concept that directing financial and operating policies enables an entity to gain economic benefits, regardless of legal ownership status. Does your company hold the ability to set and implement operating policies? If so, it can likely influence and reduce GHG emissions directly. Following this approach, your company will account for 100% of emissions from operations determined to be under its operational control.

Operational Boundaries

Once organizational boundaries have been set, those boundaries are used to determine the operations and sources generating emissions. Emissions sources are designated as either direct or indirect. Direct emissions sources are owned or controlled by the company. In contrast, indirect sources are considered a consequence of the activities of the company.

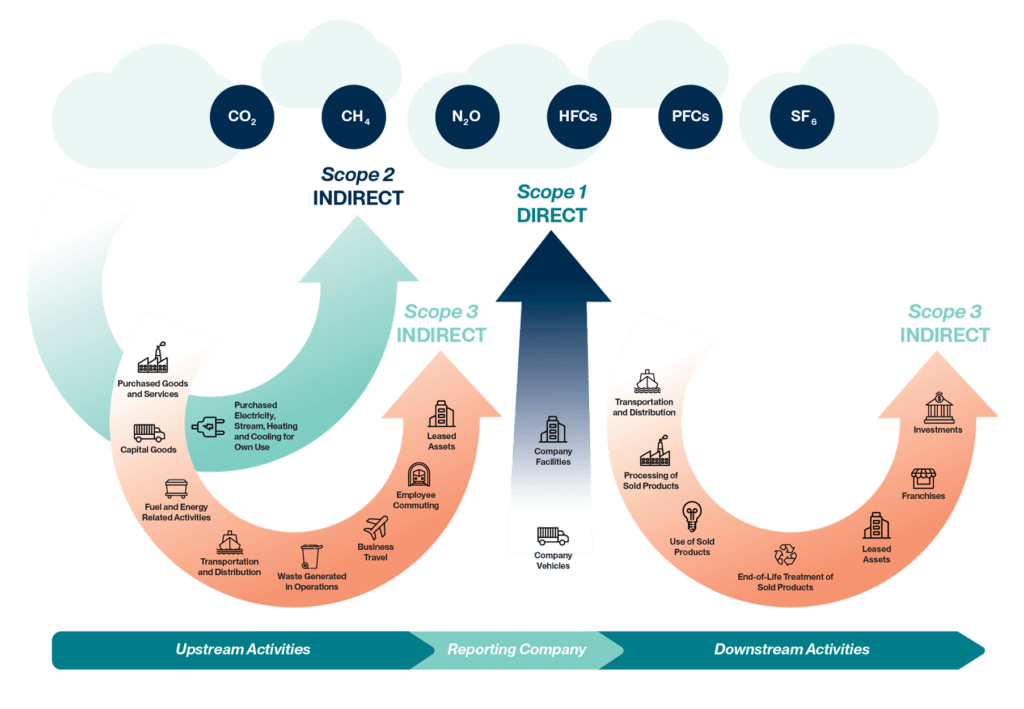

Measuring Emissions by Scopes and Activities

In alignment with the GHG Protocol, emissions are grouped together under three scopes and 15 categories. Direct emissions, also known as Scope 1 emissions, originate from things like fuel combustion in company-controlled vehicles and facilities, as well as fugitive emissions. Scope 2, or indirect emissions, are those that usually occur at a power plant not owned or controlled by your company. This includes purchased electricity, heat, or steam.

Scope 3 emissions, arising from the value chain, tend to house most emissions that comprise an organization’s GHG inventory. The Carbon Disclosure Project’s Global Supply Chain Report 2022 highlighted that Scope 3 category emissions accounted for a magnitude of 11.4 times greater than direct emissions. Scope 3 emissions are divided into 15 distinct categories incorporating value chain activities that are characterized as being either upstream or downstream.

Characterizing Emission Categories

Upstream emissions categories correlate with activities related to suppliers and internal operations. Downstream emissions categories include activities tied to customers and the full lifecycle of products, such as the product-use phase and the end-of-life treatment phase, in addition to leased assets, franchises, and investments.

Depending on whether your company manufactures a physical product or provides professional services, certain categories will likely have greater relevance than others. For a consumer-packaged goods (CPG) company, for example, purchased goods and services will entail looking at purchase orders or bills of materials to determine the emissions resulting from the inputs used to make the final product.

On the other hand, this category for a professional services firm would encompass office supplies, including paper products, as well as consulting or marketing services. For a CPG company, transportation and distribution may constitute a significant proportion of emissions, while for a service provider, their major contributors would be employee commuting and business travel.

Figure 1 – Overview of GHG Protocol scopes and emissions across the value chain

Corporate Value Chain (Scope 3) Accounting and Reporting Standard, GHGP, WRI, wbscd

Regarding data collection practices, organizations should prioritize collecting actual physical or activity data over monetary spend, as it allows for heightened granularity and accuracy in calculating emissions. “De minimis” levels are used to determine whether an error or omission is a material discrepancy or not. Once data is collected from your organization, as well as important suppliers and partners, calculations can begin.

The foundational equation for Greenhouse Gas accounting is: Activity data x emission factor = emissions. Emission factors then convert activity data to emission values.

Verifying GHG Reports

According to the GHG Protocol Corporate Standard, organizations should choose a base year for which verifiable emissions data is available. There is a wide range of voluntary disclosure frameworks, depending on your report’s target audience. Some CPG brands might receive supply chain survey requests from their distributors through CDP, while others might benefit from the direct consumer-facing Climate Neutral Certified label and publish findings in their annual impact report.

In some instances, a third-party verifier may be required to validate the GHG inventory report. To prepare for success, best practices for GHG accounting align with the following principles: relevance, completeness, consistency, transparency, and accuracy.

GHG Accounting and Climate Action

After conducting a GHG accounting inventory, it’s time to set GHG emissions reduction targets and develop a climate action plan. Target-setting through such organizations as the SBTi (for larger businesses) or SME Climate Hub (for small-to-medium sized businesses) can ensure a level of rigor and alignment with science-based approaches deemed necessary to decarbonize the global economy by 2050 at the absolute latest.

An essential follow-up to target setting is the creation of actionable plans to reduce emissions. This provides the opportunity to engage with your employees, suppliers, consumers, and the broader community. Through in-house expertise, and relationships with expert partners such as Climate Neutral, we are well positioned to support your organization on its climate action journey. Contact our sustainability team for more information.

Sustainability is reshaping the corporate landscape and changing how companies operate and make decisions. Integrating environmental, social, and governance (ESG) considerations into business strategies and operations is imperative for building a regenerative and just economy. It’s also critical for successfully attracting talent.

By 2025, an estimated 27% of the workforce will be Gen Z (people born between the late 1990s and early 2010s). This generation brings higher expectations to work on topics like work-life balance, environmental and social justice, and mental health support.

Talent scarcity is still a massive issue for most organizations. However, by leveraging sustainability practices and other social initiatives, companies can differentiate themselves and attract the post-millennial generation.

Understanding the Mindset of Gen Z

Younger generations have distinct values that influence their career choices. Having been exposed to an endless stream of news regarding the impacts of climate change and social injustice since birth, it’s not surprising they place a significant emphasis on environmental and social responsibility. Aligning these principles with their work is crucial to Gen Z as they strive for a broader sense of purpose in their careers.

Climate anxiety is highest among Gen Z, which increasingly distrusts institutions they view as having largely failed to address this crisis. They are not motivated by statements or words, but by action. It is not enough for them to work for a company who claims a commitment to sustainability and social justice; they want to see concrete evidence and are less forgiving of companies that do not follow through on their commitments.

The Appeal of Impactful Companies

From energy conservation and waste reduction to sustainable sourcing, Gen Z is looking to support companies that actively demonstrate their efforts to minimize or mitigate their environmental footprint.

Similarly, companies that prioritize diversity, equity, and inclusion (DEI) are highly attractive to Gen Z and younger generations. A recent poll conducted by TalentLMS revealed 77% of Gen Z individuals are interested in working for a company that prioritizes DEI. Therefore, it is crucial for companies to demonstrate their commitment to social causes, environmental sustainability, and purpose-driven work to entice the latest pool of talent.

Companies that prioritize sustainability offer more than just a job. They provide a sense of purpose by taking on important societal and environmental challenges through impactful projects. These companies also offer ample opportunities for personal growth, learning, and career advancement in sustainability-focused roles. It’s no wonder that Gen Z and new job-market entrants are drawn to these positions, as they allow individuals to make meaningful contributions while advancing their careers.

Communicating Sustainability Efforts to Gen Z

Regardless of where you are in your sustainability journey as an organization, it’s crucial to communicate these efforts effectively. Authenticity and transparency are key here. Your company’s website, job postings, and social media platforms need to show an ongoing commitment to sustainability initiatives and goals. Moreover, public sustainability reports demonstrate accountability and transparency to potential applicants and job seekers.

Your company can also share employee testimonials and stories. These highlight the fulfillment that comes from engaging in your sustainability efforts and demonstrate the importance of individual contributions to your overall success.

Utilize Collaboration and Partnerships

A valuable way to attract and retain sustainability-conscious job seekers is through partnerships with universities. Establishing an internship program that focuses specifically on your impact initiatives is a powerful way to provide hands-on experience to students and recent grads, and to attract emerging talent.

Engaging with other values-aligned organizations at industry events and conferences can also foster collaboration and help establish your company as a leader in your field. Moreover, supporting sustainability-related initiatives through sponsorships and partnerships enhances your brand reputation. Also, it helps you attract top talent by showcasing your commitment to making a positive impact on the environment and society.

Welcoming Sustainability for Talent Attraction

Overall, companies that prioritize sustainability and ESG practices gain a competitive advantage in attracting top talent, especially among Gen Z. These individuals value employers who demonstrate a genuine commitment to ethical practices and personal growth opportunities.

To attract and retain sustainability-conscious individuals, organizations should integrate sustainability into their branding and recruitment strategies, which can build a positive brand image rooted in social and environmental stewardship.

In today’s rapidly evolving business landscape, employees look at companies with a discerning eye and pay close attention to how they incorporate sustainable practices into their daily operations. As a business, sustainability serves as a tool by which we measure our impact and it offers a path to assess the interconnectedness of environmental responsibility, social well-being, and economic growth. Ultimately, it sets us apart from other businesses and confers our potential competitive advantage.

Employees want to have a mission worth championing. At the same time, employers are seeking a stable, talented workforce to enhance the company’s ability to adapt to changing market conditions. There’s symbiosis in the relationship between increased sustainability efforts and employee retention. For employers, finding strategies to optimize sustainability offers employees a mission and purpose worth latching onto. Simultaneously, it enhances loyalty and commitment to the company.

The Link Between Sustainability and Employee Retention

More than ever, employees want to have their identities and values aligned with how their company does business. Concurrently, employers are responsible for keeping their employees satisfied, engaged, and productive — all of which can be leveraged through internal sustainability initiatives.

This commitment requires companies to look internally and understand what matters to their employees and stakeholders. By leveraging sustainable business practices that are material, companies can demonstrate their dedication to making a positive difference. This helps attract employees who want to be part of that mission, which, in turn, strengthens the company’s brand, reputation, and value alignment.

Creating a Sustainable Work Environment

Furthermore, effective employee retention can be enhanced dramatically by a company’s ESG (environmental, social, and governance) initiatives. With a warming climate and heightened awareness surrounding social and environmental issues, employees want to know that their company is doing its part in fostering a diverse and eco-friendly space.

Employee Input and Energy Efficiency

How can this be achieved? Ask your employees what changes they want to see. Implementing energy-efficient equipment in physical workspaces, utilizing renewable energy sources, encouraging waste reduction, and recycling are great places to start. Employers can also offer incentives for sustainable transportation, such as carpooling and public transit, or eliminate the commute altogether by encouraging remote work options.

Social Well-Being and DEI Initiatives

On the social side, companies can promote work-life balance by discussing the importance of setting boundaries, offering mental health initiatives, and subsidizing wellness programs. Arguably most important, is setting DEI (diversity, equity, and inclusion) targets, emphasizing the value of an inclusive work environment that respects and celebrates differences.

Empowering Employees for Sustainable Success

Investing in your employees can provide substantial benefits to your company and can be critical to long-term success. High employee turnover, for instance, not only results in a financial loss but also a loss of valuable institutional knowledge. By focusing on retaining talented individuals, companies can reduce recruitment and training expenses and allocate resources to initiatives that promote long-term growth and innovation.

One important way to invest in your employees is to offer tangible growth opportunities. By encouraging employees to take on leadership roles, learn new skills, and increase their responsibilities, they become more confident, efficient, and effective individuals. Simultaneously, employers eliminate the risk of stagnation and disengagement among their staff.

In the quest to retain talent, prioritizing employee development serves as a distinct commitment to nurturing the well-being of your staff and the overall growth of the company.

Promoting a Sustainable Corporate Culture

An African proverb says, “If you want to go fast, go alone. If you want to go far, go together.” Achieving a strong sense of company culture and togetherness is essential in retaining talent and fostering a sense of loyalty within your team. Ultimately, this sentiment is set by leadership (the tone from the top). Upper management plays a large role in eliminating silos within the company and ensuring congruency between departments and people.

Above all else, employers must recognize that their teams have lives outside of their jobs. Their employees need to know their free time is valued just as much as the work they produce internally. Offering flexible hours and challenging the 9-to-5 schedule can be pivotal in retaining talent and cultivating trust. In addition, taking breaks from work can result in enhanced creativity, productivity, engagement, and loyalty in the workplace.

Join the Movement

Profits don’t have to come at the expense of a company’s stakeholders and employees. Investing in your employees is mutually beneficial to your organization. At the end of the day, happy employees produce better work.

By cultivating a work environment that encourages personal growth, loyalty, and longevity, organizations can enhance their adaptiveness to market changes and maintain a competitive edge while simultaneously retaining their valuable workforce.

As stakeholder and regulator expectations grow for standardized environmental, social, and governance (ESG) disclosures and metrics, accounting firms have a tremendous opportunity to help clients through ESG compliance, assurance, strategy, and implementation engagements.

As CPAs, our professional integrity, skepticism, and responsibility for quality, as well as our understanding of the companies we serve, positions us as the ideal provider of ESG and sustainability services.

Even small ESG engagements can get your foot in the door with a business you have been courting for a while and open the opportunity for tax and audit work. ESG frameworks will have you digging into the corners of your client’s operations in a way that will help you unearth additional service opportunities you can offer, including specialized services such as service organization controls (SOC) reporting or research and development (R&D) tax credits.

Assurance Opportunities

A global benchmarking study by the International Federation of Accountants, The State of Play in Sustainable Assurance, exposed an excellent sustainability assurance opportunity for accounting firms. The report examines which companies are making sustainability disclosures and obtaining assurance on them. Additionally, it records the assurance standards firms are using and which of them are providing the assurance.

The report notes: “With investors increasingly incorporating sustainability matters into their asset allocation decisions, low-quality sustainability assurance is presenting a significant, global investor protection issue.” Of the 91% of organizations making sustainability disclosures, only 51% gain outside assurance. In many cases, that assurance is provided by consultants or others rather than by independent professional accountants.

The critical takeaway from the report is that while the regularity of reporting ESG information is high, the current prevalence of assurance is not. Our profession has the unique combination of skills, qualifications, experience, and professional ethical obligations to bring the confidence investors expect.

Reap the Benefits of Starting Your ESG Journey

The best way to enter this practice area is to take your firm through its own ESG journey. Measuring your firm through a few frameworks provides several benefits. Doing so helps you:

Identify your firm’s ESG risks and opportunities.

See each framework’s impact firsthand on your business’s operation.

Educate your firm’s stakeholders (owners and employees) on the relevance of ESG frameworks within a familiar business model.

Provide an authentic story to tell clients that can help you sell these services.

Assessing firm performance through an ESG framework will allow you to look at processes and procedures from a new perspective. Engaging in this work will boost employee attraction and retention. It can also lower attrition and increase productivity for existing employees through greater social credibility.

What Are the Risks of Not Taking a Sustainable Mindset?

Neglecting to perform this work on your firm can turn away prospects looking for a genuine ESG-minded service provider, and leave your firm exposed to its own ESG risk. Both factors can harm your bottom line, hinder growth, or detract from your recruiting efforts.

Industries and businesses taking on ESG initiatives are more likely to engage with a firm that has a strong ESG ethos. In 2021, PwC published a survey stating that more than 75% of consumers say they are more likely to buy from a company that stands up for environmental (80%), social (76%), and governance (80%) issues.

Another consideration to beginning an ESG practice without doing your own ESG reporting is the potential of creating the reputational risk of making false or misleading claims. The best way to mitigate this risk is to publish an ESG impact report showing where you stand in your journey.

Building Your ESG Practice?

If you are struggling to find enough accountants to complete your compliance work, you might worry how you’d staff a new practice area. Here is some good news: If you hire talent with a background in sustainability, you’ll add credibility to your ESG practice at the same time. These professionals can help fill the knowledge gaps for accountants. Look for individuals with environmental science or corporate sustainability degrees.

We’ve hired a sustainable management MBA, a sustainable innovation MBA, and a marine biogeochemist for our team. We have also had staff bolster their credentials with a Fundamentals of Sustainability Accounting (FSA) Credential from SASB or a Sustainability Excellence Credential from the International Society of Sustainability Professionals (ISSP).

There is opportunity in ESG, no matter the size of your firm. Do not feel like you must shoulder all the services in-house. Look to partner with other service providers, after appropriate due diligence, to expand your offerings, particularly outside the accounting industry. In addition to service offerings, look to utilize those partnerships for co-developed webinars, white papers, in-person speaking engagements, and similar opportunities. Leverage their reputation and brand to bolster your identity within the sustainability space.

Building Eminence and Embracing the ESG Opportunity

As with building any new practice, forging eminence within a space can take time. You can advance more swiftly by thinking outside the box for talent acquisition and undertaking the process first. In the end, firms need to undertake this work for the same reasons as our clients—to mitigate risk, prepare for new federal and state disclosures, meet consumer demand, improve talent acquisition, and bolster brand reputation.

In recent years, supply chain issues and talent shortages have been the main challenges to conquer, capturing most of the attention. However, sustainability is now emerging as one of the biggest disrupters in the business world. It is one of the most significant opportunities in the accounting world in a very long time. There’s no better time than now to focus on your ESG efforts.

For questions or more information on how ESG impacts business, contact Jennifer Harrity, Director of Sustainability at Sensiba.