Understanding your objectives, identifying organizational risk, enlisting executive support, and evaluating internal controls are among the keys to developing an effective internal audit function.

Internal audit provides the company, on an ongoing basis, with insights into its performance, policies, and procedures that can improve operational, compliance, and financial risks. Common objectives for an internal audit include:

Identifying and mitigating organizational risk

Enhancing financial processes and regulatory compliance

Testing the design and operation of internal controls and correcting any deficiencies

Create the Blueprint for Your Internal Audit Program

The first step in developing an effective internal audit function is developing a framework that defines management’s needs and expectations. This will vary depending on the company’s industry but will typically include examining the various categories of risk the organization faces, as well as any specific compliance requirements.

This step should be followed by conversations with leaders in different business units — finance, planning, operations, the audit committee, and others — as the first stages of a broader risk assessment. This will involve asking questions about the organization’s risks and whether the implications of a given risk are material.

You can’t eliminate risk completely, but instead, you want to develop a cross-functional view of the appropriate thresholds, so you’re devoting time and resources most effectively during the internal audit.

Deciding Who Will Lead the Audit

It’s also important for the organization to designate an executive sponsor of the internal audit function to highlight unequivocally the organization’s commitment to compliance and ethical behavior. Everyone participating in or supporting the audit needs to understand the organization will accept any findings and address shortcomings discovered during the audit process. If people believe the audit will not result in action, the process can become an unproductive exercise that wastes time and money.

Define Scope

Together, these steps will help the company define the scope of the internal audit and optimize management’s risk tolerance, as well as the thresholds for testing during the audit. For example, reviewing the approval of $49 transactions may not be an appropriate use of internal audit’s time.

This discussion also will help you design the objectives and attributes of the tests you will perform during the audit process. This may include, for example:

Interviewing process owners about their role.

Observing processes and procedures to understand whether they are performing as designed.

Reviewing documentation for completeness and accuracy.

Reconciling accounts to make sure transactions and amounts match.

Find the Best Time to Conduct the Internal Audit Procedures

The next step is scheduling time with management, process owners, and other key participants to align the audit process with the organization’s calendar to avoid intrusions during busy seasons or other important periods. You probably can’t eliminate the perception that the audit is interrupting routine work, but working to accommodate peak periods will improve cooperation and the effectiveness of the audit overall.

With this plan in place, you can launch an internal audit process knowing that it’s backed by a carefully designed, well-reasoned plan that’s aligned with the company’s financial, operational, and compliance risk management objectives.

We Can Help You with Your Auditing Needs

Whether you’re looking to establish, enhance, or outsource your internal audit function, we provide ‘right-sized’ audit support to assist you. For more information about optimizing the value of your SOX investment, reach out to our team.

Technology companies often operate at a loss, especially in their early stages, as they work to develop their product or service and grow their revenue. When this is the case, the company’s auditor will likely place a heavy emphasis on evaluating the company’s going concern disclosures.

Auditing Standards Related to Going Concern

To remain a going concern, a company must have the resources to continue its operations for the foreseeable future. Financial statements are generally prepared using the assumption that a business will continue to be a going concern.

Management is required to assess whether there are existing conditions that raise substantial doubt about the company’s ability to continue as a going concern. If substantial doubt exists, management must evaluate its plans (and the effectiveness of those plans) to alleviate this risk. This assessment will then be evaluated by the company’s external auditor.

The going concern assessment should be based on whether it is likely the company will not be able to fulfill its obligations within one year of the date the financial statements were issued.

What are Going Concern Disclosures and What is Required?

Under U.S. accounting standards, certain disclosures are required if any conditions give rise to substantial doubt about the company’s ability to continue as a going concern. The disclosures should include:

Events and conditions that raise substantial doubt.

Management’s evaluation of the significance of such conditions with the company’s ability to meet its obligations.

Management’s plans to mitigate the conditions that raise substantial doubt.

If management’s plans do not alleviate the substantial doubt, the disclosures must also include a statement that there is substantial doubt about the company’s ability to continue as a going concern. In this circumstance, the audit report will also include an emphasis on the matter paragraph regarding the existence of substantial doubt.

The Information Needed to Audit Management’s Going Concern Assessment

A company’s auditor will be required to obtain appropriate evidence to evaluate management’s assessment regarding its ability to remain a going concern. To obtain this evidence, an auditor will likely request the following information from management:

A financial forecast that extends at least 12 months from the expected issuance of the financial statements

Budget–to–actual reports for the year under audit

The most recent bank statements available

The most recent interim financial statements available

Discussions with management

We Can Help

If your business needs assistance regarding your going concern disclosures or assessment, contact us. Our auditors can help you understand how the assessment will affect your financial statement disclosures.

Resources | Insights | IRS Offers Updates For Schedule K-2 and K-3 on Form 1065

In December 2022, the IRS finalized partnership instructions for filing and furnishing Schedules K-2 and K-3 for tax years beginning in 2022, including the addition of a new exception for domestic U.S. partnerships. This article summarizes what you need to know.

What is the purpose of schedules K-2 and K-3?

Schedules K-2 and K-3 were designed to increase transparency and clarity on reporting relative to a partnership’s international activities to better enable partners to report foreign income, deductions, credits, or other relevant items on their tax returns.

In tax years prior to 2021, investment partnerships with international activities often provided relevant international tax information through disclosures created in various forms, including footnotes, supplemental schedules, and pro forma documents attached to Schedule K-1. With the release of Schedules K-2 and K-3, partnerships use these schedules to provide relevant international tax information in a standard format.

The new schedules require more detailed reporting than partnerships have been providing previously, which was necessary for them to accurately complete their own returns.

Who needs to file the forms?

In general, partnerships with international activities or foreign partners should carefully review the form instructions to determine the filing requirements with Schedules K-2 and K-3.

Schedule K-2 filers

Schedule K-2 is an extension of Schedule K of Form 1065 and includes the below-listed 11 parts to report items of international tax relevance for the partnership.

Part I, Partnership’s Other Current Year International Information

Part II, Foreign Tax Credit Limitation

Part III, Other Information for Preparation of Form 1116 or 1118

Part IV, Information on Partners’ Section 250 Deduction With Respect to Foreign-Derived Intangible Income (FDII)

Part V, Distributions From Foreign Corporations to Partnership

Part VI, Information on Partners’ Section 951(a)(1) and Section 951A Inclusions

Part VII, Information To Complete Form 8621

Part VIII, Partnership’s Interest in Foreign Corporation Income (Section 960)

Part IX, Partners’ Information for Base Erosion and Anti-Abuse Tax (Section 59A)

Part X, Foreign Partners’ Character and Source of Income and Deductions

Part XI, Section 871(m) Covered Partnerships

Schedule K-3 filers

Schedule K-3 reports partners’ allocable shares of items reported on Schedule K-2. The form includes one part in addition to the parts in Schedule K-2 (Part XIII, foreign partner’s share of deemed sale items on transfer of partnership interest).

IRS Update: Domestic Filing Exception

For partnerships with activity exclusively within the United States, the biggest update to their filing requirements is a Domestic Filing Exception that exempts partnerships with solely domestic activity and U.S. partners from filing a Schedule K-2 or K-3.

Based on the schedule’s purpose of promoting consistency in reporting items of international tax relevancy by standardizing forms and instructions, the IRS recognized that partnerships with solely domestic activity and U.S. partners generally don’t need to prepare these schedules.

To qualify for this exemption, a partnership must meet each of the following criteria:

It must have no (or limited foreign) activity during a domestic partnership’s tax year 2022. For the domestic filing exception, foreign activity means foreign income taxes paid or accrued, foreign source income or loss, ownership interest in a foreign partnership, corporation, branch, or ownership interest in a foreign entity that is disregarded as an entity separate from its owner.

During the tax year 2022, the partnership’s direct partners must be individuals that are U.S. citizens or resident alien partners, domestic decedent’s estates or trusts with solely U.S. citizen and/or resident alien individual beneficiaries, S corporations with a sole shareholder, or single-member LLCs where the LLC’s sole member is one of the persons listed above.

It must provide partner notification. With respect to a partnership that satisfies the first two criteria, partners must receive a notification that they will not receive Schedule K-3 unless upon request from a partner.

The partnership must not have received a request from any partner for Schedule K-3 information on or before the one-month date before the partnership files Form 1065. For tax year 2022 calendar year partnerships, the latest 1-month date is August 15, 2023, if the partnership files an extension.

If a partner wants to receive a Schedule K-3, they must request it from the partnership. If a partnership receives such a request on or before the one-month date, the partnership does not satisfy the fourth criterion and is therefore required to file the Schedules K-2 and K-3 and furnish the Schedule K-3 to the requesting partner.

Please note that the partnership is only required to complete, file, and furnish to the requesting partner the Schedules K-2 and K-3 parts relevant to the requesting partner; the partnership does not need to complete any other parts or sections of the Schedules K-2 and K-3.

Countless factors influence a person’s decision to purchase a particular vehicle. Everything from whether to buy a car, truck, or SUV to smaller factors, such as specific options and color. While tax considerations may not top the list for personal vehicles, certain qualities do influence tax deductions for business vehicles.

Car Deductions 101

Generally, when a vehicle is purchased, its cost is not allowed to be deducted in full during the year of purchase. Instead, the cost must be deducted, or “depreciated,” over a few years (generally five). However, there are several tax strategies for business vehicles that business owners might use to accelerate depreciation.

Some considerations include Section 179, bonus depreciation, Gross Vehicle Weight Rating (GVWR), and others.

Bonus Depreciation vs. Section 179

Section 179 and bonus depreciation are separate deductions that can be taken alone or together to help reduce a business’s tax liability.

Section 179

Section 179 deduction allows qualified taxpayers to deduct part or all of the cost of certain vehicles in the first year of business use. It is most common for Section 179 to be applied first. However, bonus depreciation may be the best option if a company has no taxable profit or the car is over the cost limit.

Bonus Depreciation

Bonus depreciation allows for an additional deduction of up to 100% of the cost of the vehicle in the first year if it is not fully deducted under Section 179. The 2017 Tax Cuts and Jobs Act increased the percentage of what could be deducted in the first year from 50% to 100%. In recent legislation, bonus depreciation began to be phased out after 2022.

Key Factors to Think About When Selecting a Business Vehicle

Gross Vehicle Weight Rating

Surprisingly, a vehicle’s weight is an often-overlooked factor while evaluating a purchase. Business-use SUVs, trucks, or vans weighing over 6,000 and under 14,000 pounds can be fully deducted in the first year.

Vans and Trucks

Consider purchasing a pickup truck with a bed at least six feet long. If purchasing a van, consider one that can seat more than nine people behind the driver’s seat. Maximize your first-year deduction with either of these factors. Sometimes, you can fully deduct the cost of the vehicle in the first year.

New vs. Used

Before the passage of the Tax Cuts and Jobs Act, there were advantages to purchasing a new vehicle instead of a used vehicle. But under the new tax law, the bonus depreciation provisions were amended to allow a deduction for used cars as well as new ones. Given this change, there is no advantage from a tax standpoint to purchasing a new vehicle versus a used vehicle.

Taking Advantage of Tax Deductions for Business Vehicle Purchases

When selecting a business vehicle, it’s important to consider all the tax implications. Get advice on deducting your business vehicle cost. Our advisors can help you find the best option for your company. Contact us today for more information about tax deductions and how they could benefit your business.

Companies engaging in business within San Francisco (“the city”) need to understand their potential obligations associated with more than 180 taxes and fees required by the city’s Business and Tax Regulations code, and to keep up with the latest regulatory changes.

In this article, we’ll review new and amended requirements under Proposition F, the Gross Receipts Tax (GRT), the Overpaid Executive Tax (OET), and the Commercial Rents Tax (CRT). Not every tax will apply to your situation, but it’s important to understand the city’s requirements and expectations to ensure timely compliance.

Understanding Proposition F

Effective at the start of 2021, Proposition F completed San Francisco’s transition away from a reliance on payroll taxes toward gross receipt taxes. The legislation eliminated San Francisco’s Payroll Expense Tax and gradually raised Gross Receipts Tax rates (discussed below) across most industries, while temporarily reducing rates for some small businesses in certain industries.

In Summary, Proposition F:

Increased the Small Business Exemption ceiling to $2 million.

Decreased the Business Registration Fee for most businesses with less than $1 million in San Francisco taxable gross receipts.

Modified the city’s Gross Receipt tax rates.

Increased the Business Registration Fee for most businesses with $1-2 million in San Francisco taxable gross receipts.

Who Is Subject to San Francisco Gross Receipts Tax?

Any person engaging in business within San Francisco is subject to the gross receipts tax. A person is considered “engaging in business” if that person (or any employee, representative, or agent of that person) conducts any of the following activities:

Maintaining a fixed place of business in San Francisco.

Owning, renting, or leasing real or personal property in San Francisco for a business purpose.

Maintaining tangible personal property for sale in San Francisco in the ordinary business.

Employing or loaning capital on property located in San Francisco for a business purpose.

Performing work, solicitation, or services in San Francisco, including operating motor vehicles on San Francisco streets in a business activity, for any part of seven or more days of the year.

Exercising corporate or franchise powers in San Francisco.

Liquidating a business when the liquidator holds itself to the public as conducting a San Francisco business.

Starting in 2022, persons other than lessors of residential real estate became required to file a return if they were engaged in business in San Francisco, were not otherwise exempt, and had more than $2,090,000 in combined taxable gross receipts.

There are exemptions for entities with limited activities within San Francisco, including:

Contracting with or acting through the San Francisco services of an unrelated investment advisor.

Maintaining formation, incorporation, or registration documents in San Francisco.

Owning an interest in a pass-through entity doing business in San Francisco.

Having trustees or directors that meet or reside in San Francisco.

Small Business Exemption Thresholds

Small businesses are exempt from payment of the gross receipts tax if their taxable gross receipts are within the “small business enterprise thresholds.” However, small businesses may still be required to register with the city and pay an annual license registration renewal fee. Every business with San Francisco gross receipts of $500,000 or more, or employees working within the city for more than seven days is required to register and pay the annual renewal fee even though a business tax return may not be required.

With respect to the tax year 2022, the small business enterprise gross receipts tax threshold is $2,090,000.

It is important to note that lessors of residential real estate have different rules for determining registration requirements and are not entitled to the city’s small business enterprise gross receipts tax exemption.

Gross Receipts Tax Rates

The gross receipts tax rates vary depending on the type of business and the annual gross receipts from business activity in the city. There are 14 different tax rates based on various business activities as determined by the taxpayer’s NAICS code. For tax year 2022, the gross receipts tax rates range from 0.053% to 0.84%. See below for a summary of 2022 tax rates by business activity category and their related NAICS code(s):

Business Activity (NAICS code)

0-$1m

$1-$2.5m

$2.5-$25m

$25m +

Retail Trade (44, 45); and Certain Services (811, 812, 813)

0.053%

0.070%

0.095%

0.224%

Wholesale Trade (42)

0.105%

0.140%

0.189%

0.224%

Manufacturing (31, 32, 33); and Food Services (722)

0.088%

0.144%

0.259%

0.665%

Transportation and Warehousing (48, 49); and Clean Technology*

0.175%

0.287%

0.518%

0.665%

Biotechnology*

0.181%

0.297%

0.537%

0.689%

Information (51)

0.573%

0.665%

0.751%

0.832%

Accommodations (721); and Arts, Entertainment, and Recreation (71)

Businesses Earning from Both SF and Non-SF Operations

Depending on the business activity, businesses must use one of three apportionment methods to determine the portion of gross receipts considered to be taxable within San Francisco:

Market: receipts are assigned to within the city if the location of the real property is in the city, if the tangible good was delivered or shipped in the city, or if the benefit of the service was received in the city.

Cost of Performance: receipts are assigned to within the city based on the percentage of within city payroll expense divided by worldwide payroll expense (unless the taxpayer has made a valid California Water’s-edge election).

Mixed: A combination of the above two methods.

Quarterly Estimated Tax Payments

Businesses are required to make quarterly estimated payments for gross receipts taxes. Businesses may apply refunds of the business registration fee and the gross receipts tax to subsequent tax periods.

The first, second, and third quarterly estimated tax payments are due and payable on April 30, July 31, and October 31 respectively of the tax year.The required quarterly estimated payments are each 25% of the prior year or current year’s tax liabilities, whichever is less. You may pay all quarterly estimated taxes at one time or individually by their respective due dates. The fourth quarter payment along with the annual return is due by February 28 of the following year.

For 2022, Residential Landlords with less than $2,090,000 in taxable gross receipts are exempt from estimated quarterly business tax payments and will not receive an estimated business tax payment notice.

Failure to pay these quarterly amounts results in a penalty of 5% of the underpayment, with no interest.

San Francisco Overpaid Executive Tax (OET)

Starting in 2022, San Francisco began imposing an additional tax on certain businesses in which the highest-paid managerial employee earns more than 100 times the median compensation of its San Francisco employees. The tax rate will increase for every additional 100 times that the managerial employee’s compensation exceeds the median San Francisco worker’s pay.

For purposes of the tax, an employee is considered to be based in the City of San Francisco for a tax year if his or her total working hours within the city during the tax year exceeds his or her total working hours in another location. Compensation includes wages, bonuses, commissions, and stock compensation.

Compensation to a part-time employee will be determined on a full-time equivalency, and compensation paid to an employee who worked for a portion of the year will need to be annualized.

As this tax is specifically designed to target large business taxpayers, taxpayers exempt from San Francisco’s GRT as a “small business enterprise” are also exempt from the OET.

Commercial Rents Tax (CRT)

The Commercial Rents Tax generally applies to lessors of commercial space in the city, and generally does not apply to businesses exempt from the GRT. This measure imposes an additional gross receipts tax of:

1% on the amounts a business receives from the lease or sublease of warehouse space in the city.

5% on the amounts a business receives from the lease or sublease of other commercial spaces in the city.

Contact Us

Don’t let confusing business tax regulations get in the way of your success in San Francisco. If you have any questions about San Francisco’s business taxes or other obligations, we are here to help.

Resources | Insights | Navigating Tax Rules for Computer Software Costs in Your Business

Do you buy or lease computer software to use in your business? Do you develop computer software for use in your business, or for sale or lease to others? Then you should be aware of the complex tax rules that apply to determine the treatment of the costs of buying, leasing, or developing computer software.

Purchased Software

Some computer software costs are deemed to be costs of “purchased” software, meaning software that’s either:

Non-customized software available to the general public under a non-exclusive license or

Acquired from a contractor who is at economic risk should the software not perform.

The entire cost of purchased software can be deducted in the year it’s placed into service. The cases in which the costs are ineligible for this immediate write-off are the few instances in which 100% bonus depreciation or Section 179 small business expensing isn’t allowed. Additionally, this applies when a taxpayer has elected out of 100% bonus depreciation and hasn’t made the election to apply Sec. 179 expensing.

In those cases, the costs are amortized over the three-year period beginning with the month in which the software is placed in service. Note that the bonus depreciation rate will begin to be phased down for properties placed in service after the calendar year 2022.

If you buy the software as part of a hardware purchase in which the price of the software isn’t separately stated, you must treat the software cost as part of the hardware cost. Therefore, you must depreciate the software under the same method and over the same period of years that you depreciate the hardware. Additionally, if you buy the software as part of your purchase of all or a substantial part of a business, the software must generally be amortized over 15 years.

Leased Software

You must deduct amounts you pay to rent leased software in the tax year they’re paid, if you’re a cash-method taxpayer, or the tax year for which the rentals are accrued, if you’re an accrual-method taxpayer. However, deductions aren’t generally permitted before the years to which the rentals are allocable. Also, if a lease involves total rentals of more than $250,000, special rules may apply.

Developed Software

Some software is deemed “developed” (designed in-house or by a contractor who isn’t at risk if the software doesn’t perform). For tax years beginning before calendar year 2022, bonus depreciation applies to developed software to the extent described above. If bonus depreciation doesn’t apply, the taxpayer can either deduct the development costs in the year paid or incurred or choose one of several alternative amortization periods over which to deduct the costs.

For tax years beginning after calendar year 2021, generally the only allowable treatment will be to amortize the costs over the five-year period beginning with the midpoint of the tax year in which the expenditures are paid or incurred.

If following any of the above rules requires you to change your treatment of software costs, it will usually be necessary for you to obtain IRS consent to the change.

Contact Us

Our team is ready to help you navigate the complex tax rules related to computer software costs and determine the most advantageous treatment for your business. If you need assistance with software depreciation or amortization, please don’t hesitate to reach out. Contact us today for more information.

ASC 842 lease accounting is effective for calendar year-end entities for the 2022 fiscal year. The core concept of ASC 842 is the intention of the FASB to move previously off-balance-sheet operating leases to the balance sheet to better reflect the contractual liabilities owed under these arrangements.

Many venture-backed early-stage startup companies, or remote-enabled companies, have minimal or no operating leases. However, this does not mean ASC 842 concepts and provisions do not need to be considered.

Four Common Misconceptions for Tech and Startup Companies

Misconception 1: No Year-End Leases Equals No Impact

The company doesn’t have any leases as of year-end, so there is no ASC 842 impact.

Truth:

This is a misconception because ASC 842 is required to be adopted as of the beginning of the period presented. Any leases outstanding as of 1/1/22 for calendar year-end entities would need to be included in the analysis of adoption and calculation of adoption entries.

Misconception 2: No Operating Leases Means No Need to Worry

The company has no operating leases and never has, so there is no ASC 842 impact.

Truth:

While the absence of traditional operating leases for office space or equipment results in no impact of adoption related to those types of leases, ASC 842 requires entities to evaluate whether there are embedded leases that were not considered under prior guidance. The FASB Master Glossary defines a lease as:

“A contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration.”

Many companies that do not have office leases may still have embedded leases with service providers that may need to be accounted for. In many cases, agreements with cloud providers for designated servers or server space (data centers and colocations) qualify as embedded leases and require capitalization.

Misconception 3: Related-Party Leases Are Like Any Other Lease

Related-party leases are evaluated the same way under ASC 842 as old lease accounting standards.

Truth:

ASC 842 requires that leases entered into with parties related to the company that are under common control are required to be assessed based on the written contract terms, regardless of the intent of the terms.

A related-party lease whereby either party may terminate the contract for convenience with no significant penalty would not have commercial substance and would not be a lease under ASC 842 as the terms are not enforceable over the specified terms. This is a change from prior guidance whereby related-party leases were evaluated for their economic substance above the legally enforceable terms and conditions.

Misconception 4: Only the Balance Sheet is Affected

ASC 842 impacts the balance sheet only and has no other significant effects after adoption.

Truth:

Companies should be diligent in considering the impact of adoption to reporting to external parties, especially banks that require financial covenant compliance, and plan proactively to inform stakeholders of any anticipated impact. Impacts on accounting and disclosure of deferred taxes should also be considered.

Companies should also ensure policies and procedures are put into place to account for new leases and contracts and any lease modifications as they occur.

Make sure to review all lease agreements, amendments, and related documents carefully and keep any changes in writing. Related-party leases should also be evaluated to ensure the contract terms in the executed lease properly reflect the intended use.

Implementing ASC 842

These are just some of the many nuances in applying ASC 842 completely and accurately to ensure GAAP compliance for technology and startup companies. If you have questions, contact our team to understand the impact on your company.

An organization’s internal controls are the rules, policies, and procedures specifying how various functions are carried out, as well as measures designed to verify those procedures are being performed effectively.

What is the Purpose of Internal Controls?

Management is responsible for developing an appropriate system of internal controls, but every employee is responsible for following and applying those practices. They are established to help an organization achieve its objectives supported by strategic, financial, and operational initiatives. At a tactical level, internal controls help organizations and management prevent errors in routine functions, reduce fraud risk, and identify and correct any problems that may arise.

Internal Control Types

Internal controls typically fall into two broad categories, which include preventive and detective controls.

Preventive Controls

Preventive controls are designed to avoid errors or misclassifications. This includes the segregation of duties designed to reduce fraud risk. For example, having someone reviewing invoices and someone else sending payments.

Detective Controls

Detective controls are designed to identify an error or misclassification after it has occurred. Common measures include records reviews, account reconciliations, and physical inventories. One example is reconciling the general ledger to various accounts, such as reconciling cash to ensure the balance on the organization’s books matches its bank balance.

Beyond a compliance focus, organizations that support strong governance, internal controls, and risk management demonstrate stronger performance than their peers that ignore these important success factors.

Components of Internal Control

A strong system of internal control will depend on identifying, establishing, and maintaining controls based on certain key components. There are several established control frameworks to aid management. No specific framework is required, and management may utilize any of their choice.

Leveraging from an established and commonly used control framework adds to the flexibility, reliability, and cost-effectiveness of management’s approach to the design and evaluation of internal controls. An example is the 2013 COSO Framework (Committee of Sponsoring Organizations of the Treadway Commission), which focuses on five components of internal control detailed below.

Control Environment

Often described as “tone at the top,” the control environment describes a set of standards, processes, and structures that provide the basis for carrying out internal control across the organization.

Risk Assessment

The risk assessment forms the basis for determining how risks will be managed. A risk is defined as the possibility that an event will occur and adversely affect the achievement of organizational objectives. Risk assessment requires management to consider the impact of possible changes in the internal and external environment and to potentially take action to manage the impact.

Control Activities

Control activities are actions (generally described in policies, procedures, and standards) that help management mitigate risks in order to ensure the achievement of objectives. These can include segregating duties, transaction review and approval, and routine account reconciliation.

Information and Communication

Information is obtained or generated by management from both internal and external sources in order to support internal control components. Communication based on internal and external sources is used to disseminate information throughout and outside of the organization, as needed to respond to and support meeting requirements and expectations. The internal communication of information throughout an organization also allows management to demonstrate to employees that control activities should be taken seriously.

Monitoring

Monitoring activities are periodic or ongoing evaluations to verify that each of the five components of internal control, including the controls that affect the principles within each component, are present and functioning.

Internal Control Function

In addition to a strong control environment, an organization should have an internal audit function (either on a staff or outsourced basis) to verify the effectiveness of its internal controls. For example, internal auditors will help management assess the design of the controls as well as the organization’s risks, and update management and the audit committee on the performance of those controls. Internal auditors can also help the organization prepare for its external audit.

Vital internal audit functions include:

Inspection: Reviewing transactions, reports, and other key documents.

Observation: Watching staff members carry out duties to ensure procedures are being followed.

Confirmation: Verifying account balances and financial statements.

What Can Weaken or Undermine Controls?

No system of internal controls is perfect. However, there are conditions that may undermine internal controls, which include:

Segregation of duties conflicts

a lack of separation of cash handling responsibilities related to physical custody, deposit, recording, and reconciling of cash

Control override capabilities

excessive access provisioned within significant applications, including an organization’s accounting system

Inherent limitations

the number of staff and/or staff knowledge and experience

Communication and monitoring must be consistent to ensure gaps in internal control do not occur. This is a task made more complex as an organization’s control environment is constantly evolving.

Internal Audit Help

Whether you’re looking to establish, enhance, or outsource your internal audit function, we provide ‘right-sized’ audit support to assist you. For more information about optimizing the value of your SOX investment or want to learn more about internal controls, contact our team.

Resources | Insights | Sale-Leaseback Accounting Considerations Under ASC 842

As organizations consider sale-leaseback transactions, they must understand the financial reporting implications under the new lease accounting standard, ASC 842.

What is a Sale-Leaseback Transaction?

A sale-leaseback transaction typically occurs when an organization sells an asset, such as real estate, and immediately (or soon thereafter) leases the asset back from the purchaser. The organization that sold the asset is now a lessee, and the buyer is a lessor.

Sale-leaseback can be a useful tool for companies that need to raise capital quickly. However, it’s important to weigh the pros and cons carefully before deciding if this strategy is right for your business.

Pros and Cons of Sale-Leaseback for Organizations

Pros

Organizations pursue sale-leasebacks for potential benefits that can include freeing up cash for operating or investing while maintaining the use of the asset, strengthening their balance sheet by using a less-costly form of financing than a debt facility, and allowing management to concentrate on their core business operations instead of worrying about maintaining fixed assets.

For buyer-lessors, these transactions can provide income over the lease term, as well as the potential to generate further returns by investing the lease income.

Cons

Potential disadvantages that sellers-lessees need to evaluate include the potential recognition of capital gains, an increased lease liability, and the removal of the sold asset from the balance sheet. For the buyer-lessor, the primary risk is potential payment default by the lessee.

Understanding Sale-Leaseback Accounting

The first considerations in accounting for sale-leaseback transactions are determining whether a contract exists and whether the transfer can rightfully be considered a sale. Under the new guidance, these factors depend on the following criteria outlined in Topic 606, Revenue from Contracts with Customers:

The parties have approved the contract

The entity can identify each party’s rights regarding the transferred asset(s), as well as the payment

The contract has commercial substance

The entity believes it will probably collect consideration

The performance obligation is satisfied with the transfer of control of the asset(s)

Under Topic 606, the transfer of control is defined by the buyer-lessor accepting the asset and assuming: Legal title, Physical possession, The risks and rewards of ownership, and An obligation to pay for the asset

The existence of a leaseback does not prevent the buyer-lessor from obtaining control of the asset. However, the buyer-lessor is not considered to have control of the asset if the leaseback would be classified as a finance lease or a sales-type lease.

Similarly, an option from the seller-lessee to repurchase the asset would preclude accounting for the transfer of the asset as a sale unless both of the following criteria are met:

The exercise price of the option is the fair value of the asset at the time the option is exercised

Alternative assets, substantially the same as the transferred asset, are readily available in the marketplace

If the transfer of the asset is determined to be a sale, the seller-lessee should:

Recognize the transaction price for the sale at the point in time the buyer-lessor obtains control of the asset along with capital gains associated with the sale, if any

Derecognize the carrying amount of the underlying asset

Account for the newly executed lease under Topic 842

Fair Value Considerations

In a sale and leaseback transaction, the sale price might be more than the fair value of the asset because the resulting lease payments are above a market rate; conversely, the sale price might be less than the fair value because the lease payments are below a market rate.

That could result in the misstatement of amounts for the seller-lessee and the buyer-lessor. In this case, the purchase price of the asset should be adjusted if the sale and leaseback occur at other than a market rate.

Determining Fair Value

Whether a sale and leaseback transaction occurs at fair value is determined by the difference between either of the following (whichever is more readily determinable):

The sale price of the asset and its fair value

The present value of the lease payments and the present value of market rental payments

Adjustment of Sale Price

If the sale-leaseback transaction is not at fair value, the asset’s sale price should be adjusted on the same basis the entity used to determine the transaction was not at fair value. The adjustment to the sales price should be accounted for as follows:

Any increase to the sale price of the asset is recorded as a prepayment of rent

Any reduction of the sale price of the asset is recorded as additional financing provided by the buyer-lessor to the seller-lessee

Companies that have not yet adopted the new lease accounting standards can elect the package of practical expedients available during the transition and not reassess expired or existing lease contracts, assuming they have been correctly accounted for previously.

Outsourcing offers unique solutions to some of today’s biggest accounting challenges. If your company is debating how to best account for its transactions, consider the advantages of outsourcing accounting.

Advantages of Outsourcing Accounting Services

1. Outsource Accounting Cost

Outsourced accountants can cost a fraction of what you pay to recruit, hire, supervise, and retain an in-house accountant. In many cases, outsourcing firms can perform the same volume, quality, and consistency of work as your own accounting team, just at a much lower cost.

2. Accessibility to Accounting Personnel

Competition is fierce for qualified accountants, making it both difficult and expensive to staff an in-house accounting team fully. As an alternative to traditional recruiting, outsourcing makes it far easier to access accounting talent, generalists, and specialists alike.

3. Timely and Efficient

Getting the accounting done correctly takes time and companies may not have the staff or inclination to invest in the proper resources. Instead of compromising, rely on an outsourced accounting firm to handle the workloads and free up hours to spend on other high-priority items.

4. Accounting Expertise

Most companies need specialized accounting insights at some point, even if they don’t need to have specialized accountants in their ranks. Outsourcing firms employ a wide range of specialists for clients to consult with as needed. Think of it as expertise on demand.

5. Financial Liquidity

Managing cash flow takes time, experience, and a careful touch. Relying on an outsourced accounting firm often improves cash flow as these firms have more time and resources to dedicate to the effort, often at a fixed fee.

6. Precise Budgeting

As the overall roadmap for the company, budgets can lead toward riches or ruin. Enlisting outsourced accountants to help prepare the budget ensures that all variables – positive or negative – have been fully considered before deciding where to spend.

7. Detailed Reporting

Understanding your results are critical to managing your business. An outsourced provider will report back to you on your operations, focusing on trends that are both positive and negative, giving you critical information to help navigate your business going forward.

8. Knowledgeable Tax Consulting

Few companies are equipped to handle their own taxes. Visiting a tax prep specialist once a year may not be adequate either. By contrast, outsourcing is a long-term partnership that utilizes a deep understanding of your finances to deliver expert tax advice whenever necessary.

9. Automation Insight and Implementation

Transform your business by working with an outsourced provider to select the best-in-class automation tools to reduce data entry and cumbersome manual processes. This will streamline operations, improve internal controls, and reduce operating costs.

Is It Time for Your Company To Start Outsourcing?

Interested to learn how these advantages of selecting an outsourced accounting service could benefit your organization? Reach out to our outsourced accounting team, and let’s discuss your goals.

While an effective internal audit function can help an organization mitigate organizational risks, identify inefficient processes, enhance compliance, and reduce the potential for fraud, it’s important to review the process itself. Reviewing the internal audit process ensures it delivers relevant insights to management and the audit committee.

The Benefits of Reviewing Your Internal Audit Process

Taking a step back from the audit’s findings and reviewing its process provides several benefits, including emphasizing the idea that an internal audit is designed to identify opportunities for organizational improvement. By examining the audit as well as the organization’s performance, policies, and procedures, management is highlighting the cultural importance of continuous improvement.

It’s valuable for the audit to be seen as a partnership and a process that adds value to the company by helping it improve, not as a policing exercise for policy violations. This perception will improve the willingness of process owners to cooperate with the audit and increase its overall efficiency.

Steps to Take During the Review Process

Go Over Internal Audit Results

A valuable first step in enhancing your internal audit process is reviewing its results and insights with company management and the audit committee — not just any deficiencies the audit may have uncovered but the overall results and information provided.

Among the questions to ask include:

Is the information provided by the audit relevant and useful?

Do you need information that the audit is not providing?

Does the overall audit plan make sense?

Is the audit evaluating the most significant organizational risks?

Examine Initial Goals

It can also be helpful to review the internal audit plan’s initial objectives. Doing so can make sure the goals that were outlined at the beginning of the process have been achieved. These conversations will be beneficial in making sure the audit is providing effective insights to its end users and filling its role in helping the organization address its financial, operational, and compliance risks.

It’s also critical to ensure that the auditors are reviewing the right information. Examining incomplete or inaccurate data will clearly hinder the team’s ability to generate meaningful insights from the audit process.

Corrective Actions to Take After Evaluating the Internal Audit Process

If deficiencies or improvement opportunities are discovered, it’s also important for the company to give people enough time to complete the necessary changes. This, of course, depends on the severity of the issue. But, in most instances, providing enough time to address an issue reduces the potential for someone to feel stigmatized and increases their trust in the internal auditors.

Finish the Cycle – Recognize that Changes Create New Risks and Opportunities

Changes, including macroeconomic, regulatory, industry space, and even work patterns (including remote work arrangements) create new risks and/or change the level of current risks. Taking time as a high-performing audit function and a team performing a current state analysis is essential to ensuring the audit function continues to evolve and provide the best service to the organization.

Whether you’re looking to establish, enhance, or outsource your internal audit process, we provide ‘right-sized’ audit support to assist you. For more information about optimizing the value of your SOX investment, reach out to our team.

ESG is becoming a significant topic in the investing and corporate world and for a good reason. But what does ESG entail? How is it different from sustainability and Corporate Social Responsibility (CSR)? And in what ways is it valuable and material to my company?

What is ESG and What Does it Stand For?

ESG is an acronym for Environmental, Social, and Governance. As businesses strive to do more than just make a profit, the concept of Environmental, Social, and Governance (ESG) has emerged. This holistic approach takes into account the impact that businesses have on both people and the planet.

3 ESG Components

Environmental

Environmental captures a company’s environmental performance and impact, which is mainly determined through a company’s greenhouse gas emissions, resource consumption, and general compliance with environmental regulations. It is mainly a framework that helps investors evaluate risk according to defined E, S, and G criteria that align with standardized global frameworks, such as the Sustainability Accounting Standards Board (SASB) or the Task Force on Climate-Related Financial Disclosures (TCFD).

Social

The social aspect of ESG evaluates the impact a company has on its employees, customers, and the greater communities in which it operates. This is typically defined by a company’s commitment to Diversity, Equity, and Inclusion (DEI), marketing, community engagement, and supply chain.

Governance

Governance is determined by an organization’s leadership and structure, such as executive compensation, shareholder voting, company considerations when making business decisions, and general transparency and accountability to all relevant stakeholder groups.

ESG vs. Sustainability

When most individuals think of sustainability, they think of the environmental movement of 50 years ago. Just as business has evolved over the last 50 years, sustainability has too. Sustainability these days encompasses social and economic issues such as quality education and healthcare for all, reducing inequalities, and eliminating poverty. The United Nations defines sustainability as meeting the needs of the present without compromising the ability of future generations to meet their own needs.

Sustainability is a much broader concept that can take a multitude of forms based on the organization. It can be seen in the form of philanthropy, reducing waste/emissions/etc., and anything that would benefit society or the planet. ESG digs into the metrics and performance using global frameworks, such as the Sustainability Accounting Standards Board (SASB) or the Carbon Disclosure Project (CDP).

ESG Business Models Example

A great example to illustrate this is to look at an oil and gas company versus a company that produces all-electric vehicles. The oil and gas company may have a high ESG score but a low-impact business model. The electric car company has a good impact business model but might score very low on the ESG scale based on how they treat their employees, for example.

There are some frameworks, like B Corporation Certification, that take both performance metrics and impact into consideration™ when evaluating a company.

Why is ESG important?

ESG reporting and frameworks help interested stakeholders understand an organization’s risk and opportunity management in these areas. The intention is to improve the business practices of a company while simultaneously boosting the company’s reputation with investors and customers. Especially during and after the tumultuous times of a global pandemic and following the economic downturn, investors tend to see companies who prioritize ESG as more resilient due to better long-term risk management.

There are infinite reasons ESG is valuable to an organization. First and foremost, companies have a moral obligation to uphold strong social values and a social conscience. More and more consumers and investors are scrutinizing organizations that behave antisocially or make empty promises, also known as greenwashing.

Besides that, prioritizing ESG can reduce costs, protect valuations, reduce regulatory infractions, and increase productivity. This is done through energy-efficiency and renewable energy strategies, staying compliant with all government regulations, attracting top talent, and decreasing employee turnover.

Tools for ESG Measurement

To reap these benefits, a company must determine what is relevant to its business success and what is important to its stakeholders. A materiality assessment is a formal process that considers an organization’s industry and size to identify environmental and social issues and informs stakeholders for strategic decision-making. It also identifies how financial targets and environmental and social performance overlap and what actions can be taken to improve both.

Materiality Assessment Options

Sensiba offers three comprehensive ESG assessment options. Impakt IQ (IIQ),SASB and B Corp Certification™. Which one is suitable for your organization ultimately depends on your organization’s needs and goals. IIQ, SASB, and B Corp set baselines and benchmarks but vary in rigor, detail, and accountability. SASB is an introductory ESG assessment, IIQ is a moderate to rigorous evaluation, and B Corp offers a third-party certification of ESG scoring and impact business model performance.

Impakt IQ Assessment

The IIQ Assessment requires 7-9 C-suite leaders and takes about 3-4 months to produce a detailed, investor-grade framework that integrates ESG metrics into a company’s DNA. This assessment is appropriate for an organization that can invest significant human and financial capital toward holistic transformation from “business-as-usual.”

SASB

SASB takes 1-3 executives and about 6-8 weeks to produce the top 5-10 Key Performance Indicators (KPIs) and a high-level strategy and roadmap for the future.

B Corp Certification

B Corp Certification takes a single executive-level sponsor and about 1-1.5 years to complete the B Impact Assessment and proceed through verification for certification. Once complete, an organization will have an ESG-type score and an impact business model score. This route is appropriate for consumer-facing companies looking for a more purpose-driven business transformation.

By understanding what ESG is and its benefits, your company can make strides in becoming a leader in responsible business practices. Good environmental, social, and governance policies result in better risk management and improved relationships with investors, customers, and employees. A materiality assessment can help you identify which areas are most important for your company to focus on. For more information on how we can help you get started, contact us today.

Contact our team for more information about the Sensiba Center for Sustainability and how we can help you on your ESG journey.

As the world evolves and the B Corp movement grows (both in size and strength), its standards must also progress to ensure B Corps are making meaningful impacts towards an equitable and regenerative economy.

At the end of 2020, B Lab announced their standards (also called performance requirements) were undergoing a review. Now that the review has been completed, the B Corp community received an in-depth look at their new requirements.

Current B Lab Standards

The current B Lab standards for B Corp Certification are relatively simple, even if the journey of getting it is complicated: earn an overall verified score of 80 and meet B Lab’s legal requirement by either amending governing documents or becoming a Benefit Corporation. While that may sound easy, any company that has ever gone through the process can tell you it’s not; it is a rigorous and comprehensive process that can take a year or more.

Despite this rigor, the current standards have their limits and challenges. In particular, the certification of many larger multinationals in recent months has put the standards under heightened scrutiny. This has called into question the certification’s accountability and effectiveness for driving positive impact.

To ensure the longevity of B Corp Certification, B Lab worked with the Global Reporting Initiative (GRI) on their new standards to fill the gaps in their reporting and make ESG reporting more consistent.

Where Standards Are Going

The new requirements call for higher accountability on climate action, social justice, equality, public health, and other pressing social and environmental issues. The new framework has ten specific topics that are applicable across industries and most relevant to the goal of creating an inclusive, equitable, and regenerative economy, listed below:

Purpose & Stakeholder Governance

Worker Engagement

Fair Wages

Justice Equity Diversity & Inclusion (JEDI)

Human Rights

Climate Action

Circularity and Environmental Stewardship

Collective Action

Impact Management

Risk Standards

The biggest change is the movement away from a simple 80-point minimum. This standard was too flexible and allowed companies that many deemed disingenuous to gain certification. Many companies can pass an 80-point threshold by leveraging a specific positive environmental or social impact while contributing negatively to another area. Now, companies must meet minimum requirements in all ten of these categories to gain certification.

Example of the New Standards

For a company to be eligible for B Corp Certification, it must track its greenhouse gas (GHG) emissions annually and implement a climate transition plan to contribute to keeping global warming below 1.5 ° under the Climate Action area. More information on the specifics of each new standard can be read here.

The new standards are much more specific and will help ensure that all B Corps are doing their part to advance important social and environmental issues. One of the issues that is most likely to cause concern for many smaller businesses is the burden of proof that these different categories may pose, greatly decreasing their chance of certification despite the fact these smaller companies are relatively low risk compared with medium to large enterprises.

What This Means for Your Certification or Recertification Process

The future isn’t certain, but our B Corp Consultants are ready for the challenge. The new standards are substantially more rigorous, but this also means the certification will have higher accountability and, therefore, favorability among consumers and investors. Establishing yourself as a purpose-driven enterprise is a key differentiator in today’s landscape. A B Corp certification is a great way to make ESG and climate action part of the DNA of your business.

Contact our team for more information about how we can help you become B Corp Certified.

Resources | Insights | The Importance of an Accounting Firm for ESG Reporting

Corporate responsibility is a growing priority and has significantly increased in importance to consumers, investors, and other key stakeholders for both public and private companies. This emerging cultural movement concerning Environmental, Social, and Governance (ESG) metrics from corporations has caused an exponential increase in the number of ESG reports conducted by companies across all sectors.

Not All Reports are Made Equally

While increased ESG reporting is generally seen as a proxy for progress, these ESG reports are often misleading, nonstandard, and imprecise. Most companies do not engage in third-party verification of their ESG reports, leading to ambiguous and incomplete data.

Due to the lack of mandatory compliance and auditing within ESG, there is a heightened risk of greenwashing, which can create significant reputational and financial risks. The lack of third-party auditors has caused many consumers, investors, and other stakeholders to be cynical concerning the reliability and validity of ESG reports, especially those completed internally.

The Importance of ESG Reporting by the Numbers

According to Natixis, almost three-quarters of investors and two-thirds of fund selectors say it is unclear which ESG-relevant data is material to investment analysis. In that same study, 71% of investors agreed that they want to make a positive social impact with their investments, and 81% said they want their investments to match their values. On top of that, 77% of fund selectors say ESG factor analysis is integral to sound investing.

Working with an Accounting Firm

Sustainability accounting improves transparency and validity, which is why using an accounting firm for ESG reporting is highly valuable. Accountants have a wealth of experience producing high-quality, audit-worthy deliverables, and these skills are transferrable to the nonfinancial aspects of a company. In the ESG field, there is a growing desire for ESG reports that mirror the compliance and regulation in financial reporting.

As regulation and auditing become more standard in reporting, having poor internal controls and inaccurate published reports can put a firm at risk. By using an accounting firm with regulatory and auditing experience in the financial aspects of business, a company can safeguard the risk of greenwashing by having audit-ready deliverables that accurately capture the environmental and social impacts and risks.

Similarities and Differences Between ESG and Financial Reporting

Presently, sustainability is seen as a buzzword rather than a well-established and defined approach. This starkly differs from financial reporting, which is held to much higher standards and regular auditing and compliance. The goal of financial reporting is to produce an accurate and detailed overview of the financial status of a company.

The same goals are present in sustainability; however, there is a notable lack of regulation. Both financial and sustainability reporting seeks to increase transparency and accountability, gain consumer and investor confidence, and improve a company’s overall reputation.

There is also a well-established link between a company’s financial performance and having stronger corporate social responsibility. Despite these similar goals, financial reporting continues to be much more standardized and regulated. The increase in third-party auditing and regulations will bring credibility to ESG reporting and increase opportunities and value creation.

How We Can Help You

Currently, private companies are not required to disclose. There is also an increasing number of retailers, investors, and consumers who want to know a company’s ESG commitments and stewardship before engaging in business to ensure this information is accurate and reliable.

It is then crucial to proactively compile thorough, accurate, and audit-worthy ESG reports sooner rather than later as market pressures continue to grow in this area. Due to the complicated nature of ESG reporting, working with an accounting firm can accelerate your business past competitors. Contact our team for more information about ESG reporting.

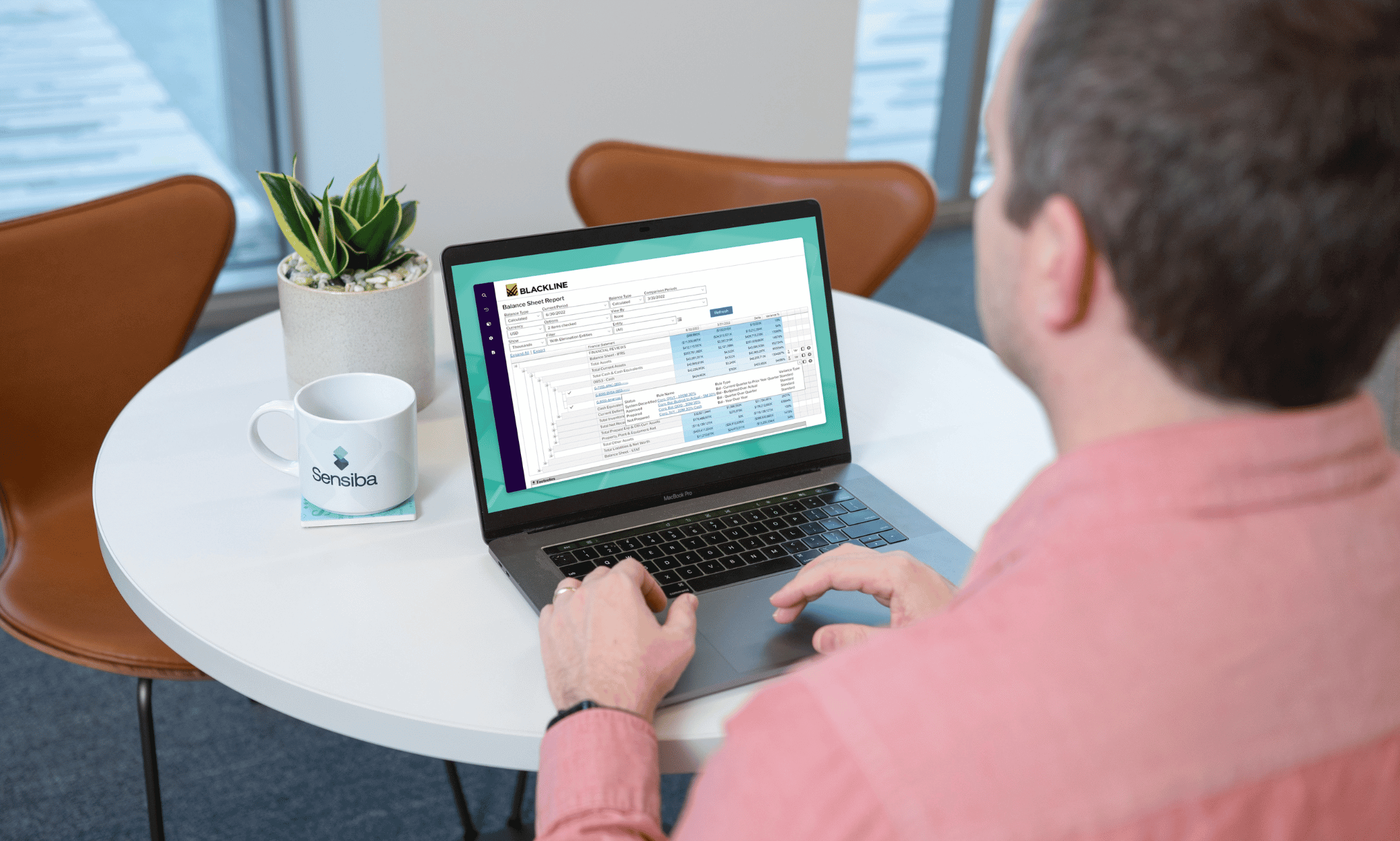

Resources | Insights | Preparing for Your First Financial Statement Audit with BlackLine

A company’s first financial statement audit can be an administrative challenge. Still, effective planning and implementation tools such as BlackLine can help streamline the process, improve internal controls, and potentially reduce audit fees.

BlackLine’s MAP Framework

BlackLine and its Modern Accounting Playbook (MAP) framework help growing and mid-sized companies optimize and automate key aspects of their financial close and financial reporting processes. These can include balance sheet and income statement reconciliations, task management functionality to help the finance team remain organized and efficient throughout the close process, and transaction matching for clearing bank to general ledger transactions.

BlackLine helps companies shift their audit preparation from a manual process driven by and reliant on spreadsheets to a largely automated exercise that helps the finance team optimize its efforts to perform quality work efficiently.

Centralized Data

One of the most powerful ways BlackLine can help a company prepare for its first financial statement audit is by enabling a centralized repository for its data. Instead of financial and performance data being stored on spreadsheets, potentially in multiple locations, BlackLine offers a secure cloud-based repository that offers a single source of truth for vital information.

Advantages of Having a Single Repository

A cloud-based repository offers several advantages for the company during the close process, as well as when it prepares for its audit. Data must no longer be compiled and reformatted manually, saving valuable staff time and effort. Additionally, here are other advantages of BlackLine’s centralized data.

Ability to Select Shared Access

The company can give its auditors access to selected data within the cloud-based repository. This can optimize the audit by eliminating the time-consuming aspect of a manual audit in which the auditor requests data that the finance team has to compile and share.

Decrease Wasted Time Tracking Down Information

Storing information in a centralized repository also reduces the risk of requested information being challenging to track down. In addition to wasting time and causing frustration within the finance team, searching for missing data can increase the time the audit takes (and create a corresponding increase in audit fees).

In contrast, being able to provide information readily reduces time and increases efficiency, as well as the auditor’s ability to rely on the company’s work. This reliance, in turn, can also help the company reduce audit fees or avoid unexpected overages.

Stronger Controls

BlackLine also helps a company establish and maintain effective internal controls over financial reporting by automatically creating and enforcing key controls such as segregation of duties. For example, a preparer will not be allowed to approve his or her work, such as an account reconciliation.

These controls are vital for all companies, but building them into a financial reporting platform is especially helpful for newer companies managing vast amounts of information during their initial financial closes and audits.

Similarly, BlackLine can help the company identify areas of the balance sheet that might be classified as high risk. Designating some accounts, such as cash, as key accounts can help the company focus on those accounts by coordinating activities among different functions or adjusting due dates to ensure control activities are enforced. Automating this monitoring helps the finance team focus time and resources on other areas.

Interested in learning more? Reach out for a demo and see how BlackLine can help automate and centralize tasks within your organization’s financial close.

Section 179 allows businesses to take a deduction for the full purchase price of qualifying equipment, vehicles, and/or software purchased in that tax year. This deduction is beneficial to businesses as it can help lower their current year tax liability. Below are answers to some of the most frequently asked questions about the tax deduction.

What is Section 179?

Section 179 of the US Internal Revenue Code is an immediate expense deduction that business owners can take for the full purchase price of qualifying equipment and/or software. Without the benefit of Section 179, business owners that purchased qualifying equipment would have to write off the purchase price a little at a time through depreciation.

Limitations on Section 179

The maximum amount that can be deducted in 2022 is $1,080,000, and that is limited to the total amount of qualifying equipment purchased, which is $2,700,000 in 2022. The deduction begins to phase out after $2,700,000 is spent and goes away completely after total purchases of $3,780,000

Qualified Businesses

All businesses that purchase, finance or lease new or used business equipment during the tax year should qualify. To qualify for the Section 179 deduction in 2022, the property must be placed in service between January 1, 2022, and December 31, 2022, and must be used for business purposes more than 50% of the time.

Eligible Property

Typically, tangible personal property such as those listed below qualifies for the deduction.

Machinery & Equipment

Office Equipment

Office Furniture

Computers

Vehicles

“Off-The-Shelf” Software

Qualified Real Property

Qualified improvement property can also qualify for Section 179. This may include improvements to the interior of a non-residential building, or external improvements like roofs, HVAC, and security systems.

Business owners must make an election to treat qualified real property, placed in service during the tax year, as Section 179 property.

Vehicles

Vehicles used in your business will qualify for the deduction with some limits. For passenger vehicles, the deduction is limited to $11,160. For certain vehicles, with a gross vehicle weight rating above 6,000 pounds but not more than 14,000 pounds gross vehicle, such as SUVs or crossover vehicles, there is a limit of $25,000.

Section 179 vs. Bonus Depreciation

Large businesses who have exceeded the Section 179 cap of $2,700,000, might consider taking bonus depreciation. Bonus depreciation allows businesses to deduct a large percentage of eligible assets immediately, rather than write off those assets over the asset’s useful life.

Bonus depreciation is not consistently offered, but it is available at 100% for 2022.

Both new and used equipment qualify for Section 179. Typically, bonus depreciation can only be taken on new equipment; however, currently, bonus depreciation can be taken on used equipment as well.

Do I Qualify for Section 179 Tax Deduction?

If you have questions about what assets might be deductible or how to claim Section 179, reach out to our team for support.