A few essential updates occurred during the California Air Resources Board’s (CARB) public workshop on Tuesday, Nov. 18, regarding the California Climate Disclosure Laws: SB 253, 261, and 219. Our team has been closely monitoring the evolution of these bills and the corresponding implementation guidance in development from CARB, as well as tracking some legal challenges. We continue to work closely with CalCPA to monitor developments to ensure our clients have the most up-to-date insights and strategies.

SB 253 Changes for 2026

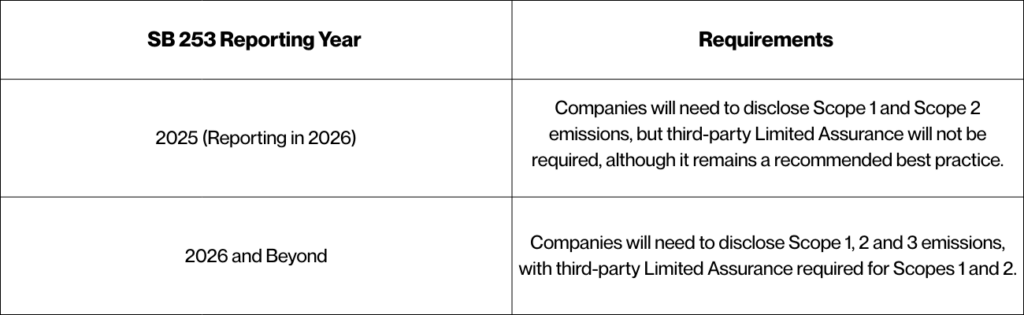

The most significant shift in implementation is regarding the Limited Assurance requirement. Initially planned for 2026, CARB staff has now recommended postponing it to 2027. Proposed changes include an extension of reporting on Scope 1 and Scope 2 emissions to Aug. 10, 2026, and exemptions for nonprofit or charitable organizations (notably, insurance companies are regulated by the CA Department of Insurance (DOI) and are excluded by statute).

Other proposed updates include the development of a flat fee structure to cover both SB 253 and 261 that would be calculated based on the annual program cost divided by the number of regulated entities

Who Does This Impact?

SB 253 and the corresponding Limited Assurance requirement apply to companies based in the U.S. and doing business in California with over $1 billion in annual revenue. CARB has refined its definition of “doing business in California” to propose only including entities whose sales exceed $735,019, and eliminating the inclusion of entities who meet payroll or property thresholds per the California Revenue and Taxation Code.

Insights on Next Steps

For many of our clients, requests for Scope 1, 2, and 3 GHG emissions data have already been rolling in for several years from large customers such as Walmart, Costco, and ALDI. This highlights the opportunity for alignment between various stakeholder requests for sustainability-related information and of having a plan in place to monitor regulatory and other compliance needs in a rapidly evolving disclosure landscape (companies in Manufacturing, Food and Beverage, and Agriculture know this all too well with the EPR laws rollout).

Focus on Data Collection and Scope 3

Building data collection processes around Scope 1, 2, and 3 data continues to be important as the Scope 3 reporting requirement is intact for 2027 under SB 253.

Prioritize 2026 Assurance Readiness

To set up for success for reporting and assurance in 2027, companies should continue their GHG emissions calculations procedures and engage in Assurance Readiness exercises in 2026.

Establish Internal Controls and Roles

Entities that use this time to build internal controls processes around GHG data and assign roles and responsibilities will be well positioned to respond to reporting requests.

Invest in Finance Team Training

We support clients with Finance Team Trainings to ensure that all material emissions sources are captured in the data collection process.

Temporary Pause on SB 261 Implementation

On Nov. 18, the U.S. Court of Appeals for the Ninth Circuit (San Francisco) issued an order which pauses the enforcement of implementation of SB 261. Arguments will be heard on the appeal on Jan. 9, 2026. Since the original Jan. 1, 2026, reporting deadline is written in statute, if requests for a longer pause are denied, then SB 261 reports will be immediately due for covered entities. (National Law Review, Nov. 20, 2025).

Who Does This Impact?

Companies doing business in California with revenue exceeding $500 million are required to publish a climate-related financial risk report aligned with TCFD or IFRS S2. First reports are due on Jan. 1, 2026, per statutory deadline.

Insights on Next Steps

Investors and other stakeholders, including employees and consumers, have heightened expectations when it comes to how companies are managing climate-related risks and opportunities.

Companies engaged in climate-related risk reporting are already realizing benefits from refined governance processes, delineated management roles and responsibilities, and established plans to address existing data collection gaps. It’s also revealing opportunities to create more proactive approaches to risk management and integration of mitigation plans into business strategy as extreme weather intensifies and impacts value chains.

SB 261 Timeline: Key Dates for Compliance

- Dec. 1, 2025: CARB will open a docket for report submissions.

- Jan. 1, 2026: Covered entities must post the report on their company website (statutory reporting deadline).

- July 1, 2026: A link to the posted report must be submitted to the CARB docket.

We have a dedicated team specializing in GHG calculations, Double Materiality Assessments, B Corp Consulting, and fractional CSO consulting. To view our full suite of service options and explore how we can tailor a compliance plan for your organization, visit our Sustainability Services Page today.