Edited by: Julien Gervreau

To manage your company’s emissions and plan reductions, you must first be able to quantify those emissions and identify their sources. The best tool for accomplishing these goals is a Greenhouse Gas (GHG) accounting inventory, which helps organizations identify opportunities for waste or cost reductions, respond to stakeholder inquiries, and prepare for changes in evolving regulatory requirements.

To the last point, the EU’s Corporate Sustainability Reporting Directive (CSRD) will require approximately 50,000 companies, including small and medium enterprises (SMEs), to start issuing sustainability reports in 2024. Additionally, the recent harmonization of ISSB standards has seen the publishing of IFRS S1 and IFRS S2, providing climate-related reporting and disclosure guidance.

Demonstrating credible contributions to climate action can also provide an advantage when seeking access to capital or differentiating your brand in a crowded marketplace.

What Is GHG Accounting?

GHG accounting is the process of measuring the emissions resulting from your company’s operations. Standardized methodologies for GHG accounting, developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), are delineated in the GHG Protocol: A Corporate Accounting and Reporting Standard. The first edition of the standard was published in 2001, with the Scope 3 Corporate Value Chain released in 2011.

The Greenhouse Gas Protocol is currently undergoing a governance restructuring to update their standards, with a goal of finalization in 2025. The intent is to ensure standards and guidance can offer a rigorous and credible accounting foundation. The International Organization for Standardization (ISO)’s 14064-1 is another framework that provides technical guidance at the organizational level for quantifying and reporting GHG emissions and removals.

The GHG Protocol Accounting Standard covers six greenhouse gases from the Kyoto Protocol. These gases are:

- Carbon dioxide (CO2)

- Methane (CH4)

- Nitrous oxide (N2O)

- Hydrofluorocarbons (HFCs)

- Perfluorocarbons (PCFs)

- Sulphur Hexafluoride (SF6)

Setting Boundaries

Boundaries are beneficial for pursuing the elusive work/life balance, and crucial to the GHG accounting process. The process begins by determining organizational boundaries – the businesses and operations owned or controlled by the company. This is particularly salient for companies that have jointly owned or controlled entities. Deciding on an approach to boundary-setting will delineate which operations, and what percentage of those operations, should be included.

Organizational Boundaries: Equity Approach Method

Companies must choose an equity share approach or a control approach. If an organization proceeds with the equity approach, they apply the percentage of equity share to calculate the company’s share of operations. For the control approach, there are two pathways: financial or operational control.

Financial Control Method

The financial control approach is predicated on the concept that directing financial and operating policies enables an entity to gain economic benefits, regardless of legal ownership status. Does your company hold the ability to set and implement operating policies? If so, it can likely influence and reduce GHG emissions directly. Following this approach, your company will account for 100% of emissions from operations determined to be under its operational control.

Operational Boundaries

Once organizational boundaries have been set, those boundaries are used to determine the operations and sources generating emissions. Emissions sources are designated as either direct or indirect. Direct emissions sources are owned or controlled by the company. In contrast, indirect sources are considered a consequence of the activities of the company.

Measuring Emissions by Scopes and Activities

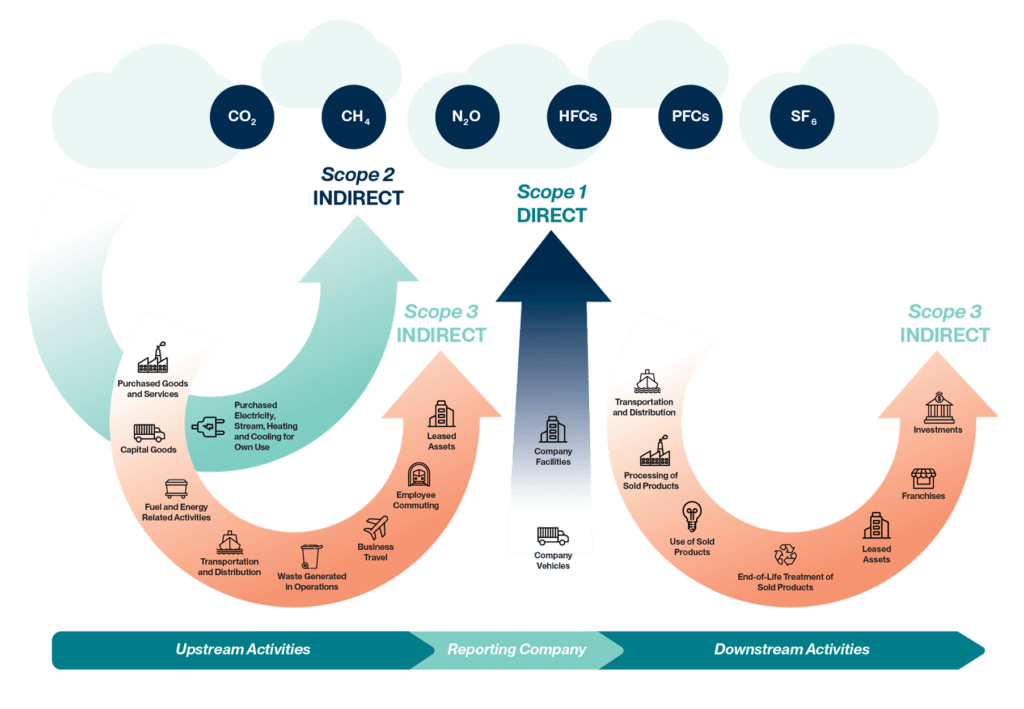

In alignment with the GHG Protocol, emissions are grouped together under three scopes and 15 categories. Direct emissions, also known as Scope 1 emissions, originate from things like fuel combustion in company-controlled vehicles and facilities, as well as fugitive emissions. Scope 2, or indirect emissions, are those that usually occur at a power plant not owned or controlled by your company. This includes purchased electricity, heat, or steam.

Scope 3 emissions, arising from the value chain, tend to house most emissions that comprise an organization’s GHG inventory. The Carbon Disclosure Project’s Global Supply Chain Report 2022 highlighted that Scope 3 category emissions accounted for a magnitude of 11.4 times greater than direct emissions. Scope 3 emissions are divided into 15 distinct categories incorporating value chain activities that are characterized as being either upstream or downstream.

Characterizing Emission Categories

Upstream emissions categories correlate with activities related to suppliers and internal operations. Downstream emissions categories include activities tied to customers and the full lifecycle of products, such as the product-use phase and the end-of-life treatment phase, in addition to leased assets, franchises, and investments.

Depending on whether your company manufactures a physical product or provides professional services, certain categories will likely have greater relevance than others. For a consumer-packaged goods (CPG) company, for example, purchased goods and services will entail looking at purchase orders or bills of materials to determine the emissions resulting from the inputs used to make the final product.

On the other hand, this category for a professional services firm would encompass office supplies, including paper products, as well as consulting or marketing services. For a CPG company, transportation and distribution may constitute a significant proportion of emissions, while for a service provider, their major contributors would be employee commuting and business travel.

Figure 1 – Overview of GHG Protocol scopes and emissions across the value chain

Regarding data collection practices, organizations should prioritize collecting actual physical or activity data over monetary spend, as it allows for heightened granularity and accuracy in calculating emissions. “De minimis” levels are used to determine whether an error or omission is a material discrepancy or not. Once data is collected from your organization, as well as important suppliers and partners, calculations can begin.

The foundational equation for Greenhouse Gas accounting is: Activity data x emission factor = emissions. Emission factors then convert activity data to emission values.

Verifying GHG Reports

According to the GHG Protocol Corporate Standard, organizations should choose a base year for which verifiable emissions data is available. There is a wide range of voluntary disclosure frameworks, depending on your report’s target audience. Some CPG brands might receive supply chain survey requests from their distributors through CDP, while others might benefit from the direct consumer-facing Climate Neutral Certified label and publish findings in their annual impact report.

In some instances, a third-party verifier may be required to validate the GHG inventory report. To prepare for success, best practices for GHG accounting align with the following principles: relevance, completeness, consistency, transparency, and accuracy.

GHG Accounting and Climate Action

After conducting a GHG accounting inventory, it’s time to set GHG emissions reduction targets and develop a climate action plan. Target-setting through such organizations as the SBTi (for larger businesses) or SME Climate Hub (for small-to-medium sized businesses) can ensure a level of rigor and alignment with science-based approaches deemed necessary to decarbonize the global economy by 2050 at the absolute latest.

An essential follow-up to target setting is the creation of actionable plans to reduce emissions. This provides the opportunity to engage with your employees, suppliers, consumers, and the broader community. Through in-house expertise, and relationships with expert partners such as Climate Neutral, we are well positioned to support your organization on its climate action journey. Contact our sustainability team for more information.